Micron – targets at 470 and 640 USD amid AI memory shortage

Micron Technology, Inc. shares delivered record revenue and issued an even stronger forecast; however, the market has begun to question the sustainability of elevated margins. The base scenario for 2026 assumes a rise in MU shares to 470 USD, followed by a move towards 640 USD after a correction phase.

Micron Technology, Inc. (NASDAQ: MU) released record Q2 results for the 2026 financial year, significantly exceeding market expectations. Revenue totalled 23.86 billion USD, compared with a consensus forecast of 20.07 billion USD, while non-GAAP EPS reached 12.20 USD versus expectations of 9.19 USD.

The company also reported non-GAAP net income of 14.02 billion USD, a gross margin of 74.9%, and an operating margin of 68.9%, representing an exceptionally high level of profitability for a memory manufacturer.

The primary driver of growth was strong demand for memory used in AI infrastructure, combined with constrained supply across the industry.

The outlook for Q3 proved even stronger than the quarterly results themselves. Micron expects revenue of around 33.5 billion USD, a non-GAAP gross margin of approximately 81%, and EPS of 19.15 USD, all of which are well above the consensus revenue estimate of 24.29 billion USD.

However, following the earnings release, MU shares began to decline as investors shifted their focus from the strength of the current quarter to the sustainability of pricing, margins, and the current memory shortage. The main negative signal was the increase in capex. Micron raised its investment plan for the 2026 financial year to more than 25 billion USD, expects around 7 billion USD already in Q3, and warned of further spending increases in 2027. The market interpreted this as an acceleration in capacity expansion and a potential normalisation of the cycle going forward.

Additional pressure came from competitors’ actions, including SK Hynix placing an order of nearly 8 billion USD with ASML to expand HBM and DRAM capacity. As a result, investors are now reassessing not Micron’s current strength, but the sustainability of its elevated profitability going forward.

This article examines Micron Technology, Inc., outlines the key sources of its revenue, summarises the company’s quarterly performance, and presents expectations for the 2026 financial year. It also includes a technical analysis of MU, which forms the basis for a forecast for Micron shares for the 2026 calendar year.

About Micron Technology, Inc.

Founded in 1978, Micron Technology Inc. is a US-based company that develops and manufactures memory chips (DRAM, NAND) and provides technology solutions for data storage. Micron is one of the world’s largest producers of electronic memory, with its products used in cars, computers, mobile devices, servers, and other electronic equipment. The company was listed on the New York Stock Exchange in 1984 and trades under the ticker MU.

Today, Micron continues to develop and deploy advanced memory modules and data storage technologies for the artificial intelligence, 5G networks, autonomous vehicle, and cloud computing markets.

Micron Technology, Inc.’s main revenue streams

Micron’s business model centres on developing, producing, and selling semiconductor memory modules and data storage solutions. The company’s segments are categorised by the product markets listed below:

- Personal computers and devices: this includes revenue from the sale of memory used in PCs, laptops, and workstations.

- Mobile devices: memory chips for smartphones and tablets, where Micron competes against companies producing comparable products for high-performance devices.

- Storage devices: products and solutions for NAND flash memory-based data storage.

- Embedded systems: memory components and modules for integration into systems used in the automotive and healthcare sectors, as well as the manufacturing industry.

The company provides detailed data for each segment and aggregates them into two major sectors in its report. The first sector is DRAM (Dynamic Random-Access Memory), which accounts for a substantial share of the company’s revenues (about 70%). DRAM is used in personal computers, servers, smartphones, graphics cards and other devices. The second sector, NAND (flash memory), accounts for about 25-30% of revenues. NAND products are used in SSDs (solid-state drives), mobile devices, data storage systems and other products that require rapid and reliable access to information.

Micron Technology Inc. Q4 2024 financial results

On 25 September 2024, Micron released its Q4 2024 report, which covered the period ended 25 August. The company’s financial performance surprised investors and exceeded forecasts. Below is the reported data:

- Revenue: 7.75 billion USD (+93%)

- Net income: 1.34 billion USD compared to a loss of 1.17 billion USD

- Earnings per share: 1.18 USD compared to a loss of 1.07 USD

- Operating profit: 1.74 billion USD compared to a loss of 1.20 billion USD

Revenue by segment:

- DRAM: 5.33 billion USD (+69%)

- NAND: 2.36 billion USD (+31%)

- Compute and Networking: 3.01 billion USD (+152%)

- Mobile: 1.87 billion USD (+55%)

- Storage: 1.68 billion USD (+127%)

- Embedded: 1.17 billion USD (+36%)

After announcing the Q4 2024 financial results, Micron’s management underscored an impressive 93% revenue growth from the previous year, driven by strong demand for DRAM products for data centres and record NAND sales, which exceeded 1 billion USD per quarter for the first time.

Micron’s CEO, Sanjay Mehrotra, noted that Micron has the best competitive positioning in its entire history and forecasted record revenue and profitability figures in Q1 2025. He also emphasised the importance of demand for artificial intelligence solutions, which helps strengthen the company’s position in the market.

Micron expects record revenue in Q1 2025, forecasting income of 8.70 billion USD (plus or minus 200 million USD) and a gross margin of 39.5%. The anticipated earnings per share will amount to 1.74 USD. These figures are considerably higher than in previous quarters, indicating growth in demand for the company’s products, particularly in the artificial intelligence and cloud computing segments.

Micron also noted that it continues to benefit from rising prices in memory and data storage markets related to increased demand for AI servers.

Micron Technology Inc. Q1 2025 financial results

On 18 December 2024, Micron published its Q1 results for the 2025 financial year, covering the period ended 28 November. Below are the report highlights:

- Revenue: 8.70 billion USD (+84%)

- Net income: 2.04 billion USD versus a loss of 1.05 billion USD

- Earnings per share: 1.79 USD versus a loss of 0.95 USD

- Operating profit: 2.39 billion USD versus a loss of 0.95 billion USD

Revenue by segment:

- DRAM: 6.40 billion USD (+73%)

- NAND: 2.32 billion USD (+26%)

- Compute and Networking: 4.40 billion USD (+153%)

- Mobile: 1.50 billion USD (+16%)

- Storage: 1.70 billion USD (+160%)

- Embedded: 1.10 billion USD (+6%)

Sanjay Mehrotra noted that data centres accounted for over 50% of revenue for the first time in the company’s history, driven by strong demand for AI memory chips. He also acknowledged the weakness in consumer segments such as PCs and smartphones but expressed confidence that growth would resume in the second half of the fiscal year.

For Q2 2025, Micron issued guidance below Wall Street expectations, forecasting revenue of 7.90 billion USD (± 200 million USD) and EPS of 1.43 USD (± 0.10 USD). This forecast reflects the anticipated decline in DRAM and NAND revenue due to oversupply and sluggish consumer demand.

Investors reacted negatively to the outlook, with Micron’s stock falling by over 13% after the report results were published.

Micron Technology Inc. Q2 2025 financial results

On 20 March 2025, Micron released its Q2 results for the 2025 financial year, covering the period ended 27 February. Below are the report highlights:

- Revenue: 8.05 billion USD (+38%)

- Net income: 1.78 billion USD (+273%)

- Earnings per share: 1.56 USD (+323%)

- Operating profit: 2.01 (+800%)

Revenue by segment:

- DRAM: 6.12 billion USD (+47%)

- NAND: 1.85 billion USD (+18%)

- Compute and Networking: 4.60 billion USD (+153%)

- Mobile: 1.10 billion USD (+16%)

- Storage: 1.40 billion USD (+160%)

- Embedded: 1.00 billion USD (+6%)

Sanjay Mehrotra noted that revenue from DRAM for data centres reached a new record. At the same time, income from high-bandwidth memory (HBM) chips rose by more than 50% from the previous quarter, exceeding 1 billion USD. He emphasised Micron’s strong competitive position and the company’s success in high-margin product categories, attributing this to an effective strategy and growing demand for memory solutions used in artificial intelligence applications.

For Q3 fiscal 2025, Micron forecast revenue of between 8.6 and 9.0 billion USD with expected EPS of between 1.47 and 1.67 USD. The company also projected a decline in gross margin to 36.5%, a 1.5 percentage point decrease from the previous quarter. This decrease was attributed to a rise in sales of lower-margin consumer products and ongoing oversupply in the NAND market, which continues to put downward pressure on prices.

Investor reaction was mixed. Following the release of the earnings report, Micron’s shares initially rose by more than 5% in after-hours trading, reflecting optimism over the strong results. However, concerns regarding the level of gross profit and rising inventory levels later led to a drop of more than 8%, making Micron one of the worst-performing stocks in the S&P 500 following the earnings release.

Micron Technology, Inc. Q3 2025 financial results

On 25 June 2025, Micron released its Q3 results for the 2025 financial year, covering the period ended 29 May. The key figures, compared with the same period of the previous fiscal year, are as follows:

- Revenue: 9.30 billion USD (+37%)

- Net income: 2.18 billion USD (+210%)

- Earnings per share: 1.91 USD (+208%)

- Operating profit: 2.49 billion (+164%)

Revenue by segment:

- DRAM: 7.07 billion USD (+50%)

- NAND: 2.15 billion USD (+4%)

- Compute and Networking: 5.06 billion USD (+97%)

- Mobile: 1.55 billion USD (–2%)

- Storage: 1.45 billion USD (+7%)

- Embedded: 1.22 billion USD (-5%)

Micron reported strong Q3 FY2025 results, significantly outperforming market expectations. Revenue reached 9.3 billion USD, up 37% year-on-year, while adjusted earnings per share rose to 1.91 USD, versus a consensus forecast of 1.60 USD. The main driver was steady growth in demand for memory used in AI systems. HBM shipments increased by approximately 50% quarter-on-quarter, and revenue from data centres more than doubled.

During the earnings call, CEO Sanjay Mehrotra noted the accelerated adoption of advanced technological solutions. Production of 1-gamma DRAM using EUV lithography began ahead of schedule, and mass shipments of HBM3E were expected as early as Q4. The company also reported the start of HBM4 testing, with plans to begin volume production in 2026. These initiatives, together with expanded manufacturing capacity in the US and government support under the CHIPS Act, were shaping Micron’s strategic advantage in the AI memory segment.

Profitability also improved, with gross margin reaching 39%, exceeding the upper end of guidance. A further increase to around 42% ±1% was expected in Q4. The company planned to allocate approximately 1.2 billion USD to operating expenses in the following quarter, with R&D in HBM and next-generation memory technologies remaining a key priority.

The Q4 outlook reflected management’s optimism. Expected revenue stood at 10.7 billion USD (+38% year-on-year), and earnings per share were projected at 2.50 USD (+111% year-on-year) – both well above analysts’ consensus estimates.

Micron Technology, Inc. Q4 2025 financial results

On 23 September 2025, Micron published its Q4 results for the 2025 financial year, covering the period ended 28 August. The key figures compared with the same period of the previous fiscal year are as follows:

- Revenue: 11.31 billion USD (+46%)

- Net income: 3.47 billion USD (+158%)

- Earnings per share (EPS): 3.03 USD (+156%)

- Operating profit: 3.96 billion USD (+126%)

Revenue by segment:

- Cloud Memory Business Unit: 4.54 billion USD (+213%)

- Core Data Center Business Unit: 1.58 billion USD (–23%)

- Mobile and Client Business Unit: 3.76 billion USD (+24%)

- Automotive and Embedded Business Unit: 1.43 billion USD (+17%)

Micron’s Q4 FY2025 results came in ahead of market expectations. The company reported record revenue of 11.32 billion USD, while adjusted EPS stood at 3.03 USD – both figures exceeding the analyst consensus of 11.2 billion USD in revenue and 2.86 USD in EPS. Revenue growth was driven by exceptionally strong demand from AI-focused data centres, which became the primary source of expansion and are now the core of Micron’s business. For FY2025, data centres accounted for 56% of the company’s revenue at high gross margins, confirming a structural shift towards higher-value, higher-margin server memory and HBM modules.

In Q4 2025, Micron improved its product mix, with more shipments of server DRAM and HBM for AI systems and fewer low-cost configurations. This shift raised average sales prices and increased margins. The memory price cycle also recovered: there was a supply shortage in DRAM, and prices for NAND also rose.

In Q4, Micron generated a positive adjusted free cash flow of around 803 million USD despite significant capital expenditures. For the 2025 financial year overall, FCF exceeded 3.7 billion USD. At the same time, management had previously warned that CapEx would rise in FY2026 as the company expands DRAM and HBM capacity to capture growing AI-driven demand.

Micron issued strong guidance for the next quarter. Revenue was expected to be around 12.5 billion USD (±300 million USD), adjusted EPS around 3.75 USD (±0.15), and gross margin in the range of 50.5–52.5%. This guidance indicated that management expected continued strength in both pricing and product cycles, particularly in server DRAM and HBM, with further potential to increase profitability as AI memory accounts for an ever-larger share of total sales.

Micron Technology, Inc. Q1 2026 financial results

On 17 December 2025, Micron released its Q1 results for the 2026 financial year, covering the period ended 27 November. Below are the reported figures compared with the same period from the previous financial year:

- Revenue: 13.64 billion USD (+57%)

- Net income (non-GAAP): 5.48 billion USD (+169%)

- Earnings per share: 4.78 USD (+167%)

- Operating profit: 6.42 billion USD (+168%)

Revenue by segment:

- Cloud Memory Business Unit: 5.28 billion USD (+100%)

- Core Data Center Business Unit: 2.38 billion USD (+4%)

- Mobile and Client Business Unit: 4.26 billion USD (+63%)

- Automotive and Embedded Business Unit: 1.72 billion USD (+49%)

Micron Technology delivered exceptionally strong results. Revenue reached 13.64 billion USD, reflecting a 57% year-on-year increase. Net income reached 5.48 billion USD, with earnings per share at 4.78 USD. The company specifically highlighted that revenue, margins, and earnings per share were above the upper end of its own guidance. The market was equally pleased, as analysts had expected revenue of approximately 12.9 billion USD and earnings per share of around 3.96 USD, and Micron exceeded both.

The quality of the quarter is evident in the strong margins. Non-GAAP gross margin grew to 56.8%, operating margin rose to 47.0%, and operating profit reached 6.42 billion USD. For the memory and storage business, these levels are very high, reflecting strong pricing power and an advantageous product mix.

Revenue growth was broad-based across all segments. DRAM revenue totalled 10.81 billion USD, growing by 69% year-on-year, while NAND revenue totalled 2.74 billion USD, up 22% year-on-year. In the quarter, DRAM prices increased by approximately 20% quarter-on-quarter, and NAND prices grew by low double digits, indicating that both price increases and product mix contributed to the profit growth. The Cloud Memory segment grew fastest, reaching 5.28 billion USD (+100% year-on-year). Mobile & Client reached 4.26 billion USD (+63% year-on-year), Automotive & Embedded reached 1.72 billion USD (+49% year-on-year), while Core Data remained at around 2.38 billion USD (+4% year-on-year).

Management's guidance for Q2 of the 2026 financial year was even stronger. The company expected non-GAAP revenue of approximately 18.7 billion USD, a gross margin of 68%, and earnings per share of approximately 8.42 USD – significantly above analysts' expectations, which had factored in much more modest figures. Looking further ahead, Micron expected further improvement in its performance throughout the 2026 financial year, planned capital expenditure of around 20 billion USD, focusing on the second half of the year. It also noted that demand from AI infrastructure and constrained production capacity wil remain key drivers of the market.

Micron Technology, Inc. Q2 2026 financial results

On 18 March 2026, Micron Technology, Inc. released its Q2 results for the 2026 financial year, covering the period ending 26 February. Below are the reported figures compared with the same period of the previous financial year:

- Revenue: 23.86 billion USD (+196%)

- Net income (non-GAAP): 14.02 billion USD (+686%)

- Earnings per share: 12.20 USD (+682%)

- Operating profit: 16.46 (+720%)

Revenue by segment:

- Cloud Memory Business Unit: 7.75 billion USD (+163%)

- Core Data Center Business Unit: 5.69 billion USD (+211%)

- Mobile and Client Business Unit: 7.71 billion USD (+245%)

- Automotive and Embedded Business Unit: 2.71 billion USD (+162%)

Micron Technology delivered record results for Q2 of the 2026 financial year. Revenue totalled 23.86 billion USD (+196% year-on-year), while non-GAAP net income reached 14.02 billion USD, or 12.20 USD per share, significantly exceeding the previous year’s figures. Notably, the results surpassed not only the company’s own guidance but also analysts’ expectations, which had projected revenue of 13.6 billion USD and EPS of around 4.78 USD.

The quality of the quarter is also reflected in profitability. Non-GAAP gross margin stood at 74.9%, while operating margin reached 69%. Operating profit totalled 16.46 billion USD, highlighting a high level of profitability driven by strong pricing and an efficient sales mix.

The main driver of this surge in performance was a combination of exceptionally strong demand for memory from AI infrastructure, constrained supply across the market, and solid execution by Micron itself. In its financial results presentation, the company explicitly stated that the sharp increase in both results and guidance was driven by rising AI-related memory demand, structural supply constraints, and strong operational performance. Management also noted that AI has effectively transformed memory from a standard component into a strategic asset, with Micron positioning itself as a key beneficiary of this trend.

The outlook for the next quarter appears even more optimistic. The company expects non-GAAP revenue of around 33.5 billion USD, a gross margin of approximately 81%, and earnings per share of around 19.15 USD. These projections significantly exceed analysts’ consensus estimates, which had anticipated more moderate results. Over the longer term, Micron plans to continue increasing capital expenditure and strengthening its position in AI infrastructure, which is expected to support further growth in both revenue and profitability.

Reasons for the decline in Micron Technology, Inc., shares

Despite record Q2 results for the 2026 financial year and a very strong outlook for the next quarter, MU shares began to decline sharply. Investors shifted their focus away from the strength of the current quarter towards the sustainability of such earnings over a longer horizon. While Micron delivered exceptional results, the key question is whether the company can maintain such pricing and margins as the industry begins to expand supply. Market participants are increasingly questioning the longevity of the current supercycle.

The primary negative signal was the sharp increase in capital expenditure. Micron raised its capex forecast for the 2026 financial year to 25 billion USD, expects around 7 billion USD already in Q3, and explicitly indicated that investment will increase further in the 2027 financial year. Moreover, the company stated that construction-related spending in 2027 will increase by more than 10 billion USD compared with the previous year. This suggests that Micron itself is accelerating the expansion of future capacity in HBM and DRAM, meaning that the current supply shortage is likely to ease over time.

The second factor relates to the structure of profitability. In Q2 2026, Micron’s non-GAAP gross margin reached 74.9%, while its operating margin stood at 68.9%. This indicates that the quarter was not merely strong, but close to an extreme phase of the cycle. Such conditions often signal not the beginning of sustained expansion, but a potential peak in profitability, after which even high-quality businesses may face margin normalisation.

Additional pressure emerged from broader industry developments following the earnings release. SK Hynix announced the purchase of equipment from ASML worth 7.9 billion USD to expand HBM and DRAM capacity, providing further confirmation that major players in the memory market are preparing to scale up production.

At the same time, Google introduced TurboQuant, a technology that can reduce the need for KV-cache memory by at least sixfold. As AI continues to evolve, improvements in computational efficiency may limit the growth in memory demand, suggesting that demand may prove less unconstrained than previously assumed.

Taken together, these factors indicate that the market is pricing in not a deterioration in Micron’s current performance, but a potentially earlier cooling of the memory cycle. However, the current reaction appears more emotional than fundamental, and over time, the market may reassess these concerns and adopt a more balanced view. This will become evident in Micron’s share price: if investor concerns persist, a downward trend may begin to form. For now, the move appears to be a correction within an ongoing uptrend.

Analysis of key valuation multiples for Micron Technology, Inc.

Below are the key valuation multiples for Micron Technology based on the Q2 results of the 2026 financial year, calculated at a share price of 357 USD.

| Multiple | What it indicates | Value | Comment |

|---|---|---|---|

| P/E (TTM) | Price paid for 1 USD of earnings over the past 12 months | 16.71 | ⬤ For a memory manufacturer, this valuation is no longer cheap, particularly after the sharp increase in earnings |

| P/S (TTM) | Price paid for 1 USD of annual revenue | 6.93 | ⬤ Valuation based on revenue is elevated |

| EV/Sales (TTM) | Enterprise value to sales, accounting for debt | 6.82 | ⬤ Even when accounting for near-zero net debt, the revenue multiple remains very high |

| P/FCF (TTM) | Price paid for 1 USD of free cash flow | 39.18 | ⬤ On an FCF basis, the stock appears expensive |

| FCF Yield (TTM) | Free cash flow yield to shareholders | 2.55% | ⬤ Low FCF yield suggests the valuation is pricing in strong future FCF growth |

| EV/EBITDA (TTM) | Enterprise value to operating profit before depreciation and amortisation | 10.76 | ⬤ For memory and NAND, this is a high multiple, even considering record margins driven by AI demand |

| EV/EBIT (TTM) | Enterprise value to operating profit | 14.11 | ⬤ Margin of safety in earnings is limited |

| P/B | Price to book value | 5.56 | ⬤ Equity is valued at a substantial premium, which is a clear signal of elevated valuation for a capital-intensive and cyclical business |

| Forward P/E | Forward price-to-earnings (P/E) ratio | 6.25 | ⬤ Based on expected earnings, the stock appears inexpensive, provided forecasts are maintained |

| Net Debt/EBITDA | Debt burden relative to EBITDA | -0.18 | ⬤ Net debt is close to zero relative to EBITDA, indicating a very strong balance sheet |

| Interest Coverage (TTM) | Ability to cover interest expenses with operating profit | 79.59 | ⬤ Interest expenses are covered with a comfortable margin of safety |

Valuation multiples analysis for MU – conclusion

At a share price of 357 USD, Micron Technology, Inc. can be viewed as an aggressively attractive opportunity, rather than an obviously undervalued stock. Based on current multiples, the company no longer appears inexpensive. However, when considering future growth, the picture becomes more compelling.

Micron maintains a net cash position, with Net Debt/EBITDA below zero and very strong interest coverage, indicating that the balance sheet does not constrain further growth. At the same time, a forward P/E of around 6.3 appears low, suggesting that the market is still pricing in future earnings relatively conservatively, despite strong demand for HBM, DRAM, and AI infrastructure.

Overall, Micron shares represent a play on the continuation of the cycle, assuming that demand for AI-related memory remains strong for longer than usual and that earnings continue to expand. If this scenario materialises, the low forward P/E could justify even the currently elevated valuation multiples.

For more conservative investors, Micron may already appear somewhat expensive. For more aggressive investors, however, the stock remains attractive, albeit primarily as a cyclical play on continued strength in memory and AI demand.

Expert forecasts for Micron Technology, Inc

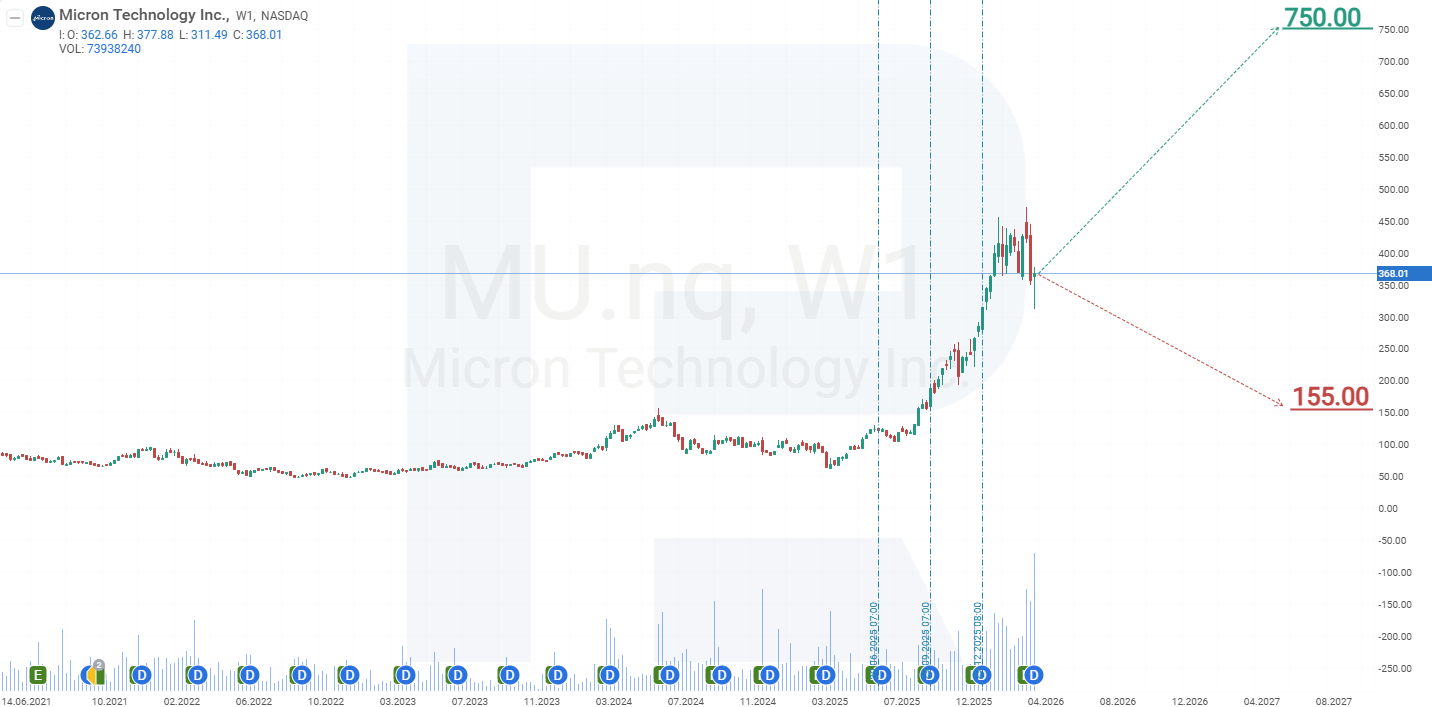

- Barchart: 31 of 41 analysts assigned a Buy rating to Micron Technology shares, including 6 Moderate Buy and 4 Hold recommendations. The upper price target is 750 USD, and the lower bound is 140 USD.

- MarketBeat: 34 of 37 analysts assigned a Buy rating to the stock, while 3 gave a Hold recommendation. The upper price target is 700 USD, and the lower bound is 155 USD.

- TipRanks: 26 of 28 analysts assigned a Buy rating to the stock, while 2 gave a Hold recommendation. The upper price target is 700 USD, and the lower bound is 400 USD.

- Stock Analysis: 11 of 31 analysts assigned a Strong Buy rating to Micron shares, 18 assigned a Buy rating, and 2 gave a Hold recommendation. The upper price target is 700 USD, and the lower bound is 150 USD.

Micron Technology, Inc. stock price forecast for 2026

Amid rising demand for memory, Micron’s revenues are increasing, and its share price has risen sharply alongside them. From April 2025 to March 2026, MU shares gained approximately 650%. Following such a strong advance, moving averages continue to indicate a sustained uptrend, while the Stochastic oscillator, in similar conditions, typically signals overbought levels.

The chart shows that the Stochastic indicator has remained in this zone for approximately 10 months, suggesting that a correction is due. Since January 2026, MU shares have been trading within a range of 357–470 USD, forming a consolidation pattern. This range can be viewed as a sideways correction that the market required after the sharp rally. A false break below support at 357 USD suggests strong investor interest in the stock and may signal potential for further upside.

Based on the current price dynamics of Micron shares, the following scenarios for 2026 can be considered:

The base case forecast for Micron shares assumes a move higher towards resistance at 470 USD. However, as the Stochastic indicator remains in overbought territory, a rejection from this level is expected, followed by a retest of support at 357 USD. Thereafter, a move higher towards 640 USD is possible.

The alternative forecast for Micron stock assumes a break below support at 357 USD. In this case, MU shares may decline to 260 USD, after which a recovery within the broader uptrend towards 470 USD would be likely.

Risks of investing in Micron Technology, Inc. stock

Investing in Micron Technology’s stock involves several risks that may adversely impact the company’s income and revenue:

- Memory market cyclicality: the semiconductor industry, particularly the memory segment, is highly cyclical, experiencing periods of fluctuating demand and pricing. A prolonged downturn in segments such as NAND and DRAM could lead to overstocking, falling prices, and reduced profitability.

- Intense competition in the industry: Micron faces fierce competition from major players like Samsung Electronics and SK Hynix. Constant investment in technology and innovation is vital in such a highly competitive environment. If the company fails to keep pace with industry developments, it may lose market share, leading to lower profitability.

- Geopolitical tensions and trade restrictions: Micron operates in the global market, generating significant revenue outside the US. Geopolitical tensions, trade disputes, and cybersecurity compliance checks may restrain sales and operations. For example, Micron’s products have been scrutinised in China, highlighting the risks tied to international markets.

Investors must carefully consider these risks when evaluating an investment in Micron Technology, as they could significantly impact the company’s financial performance and stock price.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.