Alphabet and its AI bet: how CapEx may affect the stock in 2026

Alphabet’s Q4 2025 report exceeded expectations for both revenue and profit, with Google Cloud emerging as the primary growth driver. However, large-scale investments of 175–185 billion USD planned for 2026 could temporarily reduce free cash flow and increase share price volatility.

In Q4 2025, Alphabet Inc. (NASDAQ: GOOG) confirmed its leadership in the AI sector, surpassing annual revenue of 400 billion USD for the first time. Google Cloud was the primary growth driver, increasing revenue by 48% and raising its operating margin to 30.1%. The implementation of the Gemini 3 model reduced AI query processing costs by 78%, while the updated search with AI Overviews features boosted revenue by 17%. The group’s operating margin slightly decreased due to one-off employee payouts and investments in Waymo, which now completes over 400,000 rides per week.

Alphabet did not provide specific revenue figures for the upcoming quarter, instead focusing on aggressive investments. The company intends to double its capital expenditure to 175–185 billion USD in 2026 to expand its AI infrastructure and develop proprietary chips. Monetisation is expected to accelerate through paid subscriptions and corporate licensing of Gemini Enterprise, alongside the geographic expansion of its autonomous taxi service following its launch in Miami.

This article examines Alphabet Inc., outlines its revenue sources, reviews its quarterly performance, and provides a technical analysis of GOOG shares, forming the basis for the Alphabet stock forecast for 2026.

About Alphabet Inc.

Alphabet Inc. was established on 2 October 2015 through a restructuring of Google, which was founded by Larry Page and Sergey Brin in 1998. Google was originally a search engine but gradually evolved into a diversified technology company, covering advertising, cloud services, mobile platforms, and other areas.

By 2015, Google’s scope and diversification had made its management increasingly complex. As a result, a holding structure – Alphabet Inc. – was established, with Google becoming one of its divisions, focusing on core businesses (Search, YouTube, and Android). At the same time, innovative projects, such as Waymo and Verily, were spun off into separate companies under Alphabet’s management.

Since the restructuring, Alphabet has replaced Google as the listed public company on the stock exchange, retaining its existing tickers (GOOGL and GOOG). Larry Page became Alphabet’s CEO, Sergey Brin its President, and Pichai Sundararajan was appointed CEO of Google.

Alphabet is listed on the stock exchange under two tickers, GOOGL and GOOG:

- GOOGL (Class A) – voting shares. Holders of these shares are entitled to vote at shareholder meetings (1 share = 1 vote).

- GOOG (Class C) – non-voting shares. These shares provide the same economic rights (dividends, capital appreciation) but do not grant holders the right to participate in the company’s management.

Alphabet Inc.’s main revenue streams

Alphabet Inc., the parent company of Google and other subsidiaries, generates revenue from several business segments. The primary sources of revenue are outlined below:

- Google services: the largest source of income, driven primarily by advertising. This includes:

- Google Search and others: revenue from advertisements placed on Google Search, Gmail, Google Maps, and other Google-owned services.

- YouTube ads: revenue from banner ads, skippable and non-skippable video ads, and overlay ads on YouTube.

- Subscriptions, platforms, and devices: revenue from subscription services, including YouTube Premium, YouTube TV, Google One, and NFL Sunday Ticket. This category also includes app sales, in-game purchases via the Google Play Store, and hardware sales such as Pixel phones, Nest and Chromecast devices.

- Google Cloud: revenue from cloud computing services, including infrastructure, platform solutions, and apps such as Google Workspace and Gemini for Cloud. Google Cloud serves corporate clients and is growing rapidly, although it still lags behind competitors such as AWS and Microsoft Azure.

- Other Bets: includes Alphabet’s ambitious ventures, such as Waymo (autonomous driving), Verily (healthcare), and GFiber (internet services), with most of the revenue coming from the latter two. Although this segment contributes less to overall revenue, it focuses on long-term innovation and often operates at a loss.

- Alphabet operations: includes small currency-related hedging revenue and other corporate activities. This is not the primary segment but includes other income unrelated to the core segments.

Advertising remains the primary source of Alphabet’s revenue, with Google services, notably Search and YouTube, leading the way. Google Cloud is a growing revenue stream, reflecting Alphabet’s commitment to developing solutions for companies, while other projects are speculative investments with a limited but increasing impact on revenues.

Alphabet Inc.’s financial position

Alphabet Inc. is in a strong financial position, reflecting both stability and strategic momentum. The company continues to deliver steady revenue growth, driven primarily by its advertising operations, particularly via Google Search and YouTube.

Alphabet closed 2024 with revenue of 350 billion USD, a 14% year-on-year increase. Net income rose by 28% to 100 billion USD.

Google Services, which include Search, YouTube, and other platforms, generated 84.1 billion USD in revenue in 2024, up 10% from 2023. The Google Cloud segment also expanded, reaching 12 billion USD, a 10% increase from the previous year.

Alphabet plans to invest around 75 billion USD in 2025, significantly higher than the 52 billion USD in 2024. The primary objective is to expand its AI infrastructure and capabilities. CEO Sundar Pichai emphasised the importance of AI across all the company’s products.

Alphabet Inc. Q1 2025 earnings results

On 24 April, Alphabet Inc. published its earnings report for Q1 2025, which ended on 31 March. The key figures are presented below, compared to the same period in 2024:

- Revenue: 90.2 billion USD (+12%)

- Net income: 34.5 billion USD (+46%)

- Earnings per share: 2.81 USD (+49%)

- Costs and expenses: 59.6 billion USD (+8%)

- Operating income: 30.6 billion USD (+20%)

- Operating margin: 34% (+200 basis points)

Revenue by segment:

- Google Services: 77.3 billion USD (+10%)

- Google advertising: 66.9 billion USD (+8%)

- Google Search & other: 50.7 billion USD (+10%)

- YouTube ads: 8.9 billion USD (+10%)

- Google Network: 7.3 billion USD (–2%)

- Google subscriptions, platforms, and devices: 10.4 billion USD (+19%)

- Google Cloud: 12.3 billion USD (+28%)

- Other Bets: 0.4 billion USD (–10%)

Alphabet’s Q1 2025 report showed resilient growth, enhancing the appeal of the company’s shares to investors. Revenue rose 12% year-on-year, driven by strong performance in its Search division, YouTube, and Google Cloud, while net profit increased by 46%.

The Search segment remains the primary source of revenue, with the rollout of AI Overviews reaching 1.5 billion monthly users, boosting engagement without undermining monetisation. YouTube continues to lead in the streaming segment, boasting a subscriber base of 270 million (across YouTube and Google One), which contributes to a steady stream of high-margin revenue. Google Cloud reported 28% revenue growth and a 17.8% margin, reinforcing the company’s strategic focus on AI infrastructure. The planned acquisition of Wiz for 32 billion USD, expected to close in 2026, will strengthen Alphabet’s cloud security position and enhance its competitiveness in the market.

Alphabet announced a 70 billion USD share buyback and a 5% increase in quarterly dividends, now at 0.21 USD per share, reflecting confidence in its outlook.

The company’s management did not provide specific guidance for Q2 2025, but the analyst consensus forecast expected revenue of 93.6 billion USD and earnings per share of 2.14 USD, indicating continued stable growth.

Chief Financial Officer Anat Ashkenazi highlighted the risks linked to tariffs, particularly affecting the advertising business in the Asia-Pacific region, but confirmed that capital expenditure in Q1 2025 (17.2 billion USD) was in line with the full-year plan. The company’s ongoing focus on innovation in Search, the expansion of its Cloud business, and the development of autonomous transport via Waymo (which now covers over 500 square miles) are creating multiple growth drivers.

Alphabet’s strong quarterly performance underscores its ability to adapt and grow even in a highly competitive environment. Its leadership in AI, continued growth in its Cloud division, and ongoing share buyback programs and dividend payouts make the company’s shares appealing to investors with a focus on future-facing technologies.

Alphabet Inc. Q2 2025 earnings results

On 23 July, Alphabet Inc. released its Q2 2025 earnings report for the quarter ended 30 June. The key figures, compared with the same period in 2024, are as follows:

- Revenue: 96.43 billion USD (+14%)

- Net income: 28.20 billion USD (+19%)

- Earnings per share (EPS): 2.31 USD (+22%)

- Costs and expenses: 65.16 billion USD (+14%)

- Operating income: 31.27 billion USD (+14%)

- Operating margin: 32.4% (+40 basis points)

Revenue by segment:

- Google Services: 82.5 billion USD (+12%)

- Google advertising: 71.34 billion USD (+10%)

- Google Search & other: 54.19 billion USD (+11%)

- YouTube ads: 9.79 billion USD (+13%)

- Google Network: 7.35 billion USD (–1%)

- Google subscriptions, platforms, and devices: 11.20 billion USD (+20%)

- Google Cloud: 13.62 billion USD (+32%)

- Other Bets: 0.37 billion USD (+2%)

Alphabet Inc. (GOOGL) delivered strong Q2 2025 results, surpassing market expectations. Growth was fuelled by the rapid expansion of AI‑related initiatives and robust demand for cloud solutions. However, the report also highlighted several challenges that weighed on investor sentiment and the short‑term outlook for the stock.

Alphabet’s revenue reached approximately 96.4 billion USD, up 14% year-on-year. Earnings per share came in at 2.31 USD, exceeding both last year’s result (+22%) and the analyst consensus estimate of 2.14 USD. These figures signalled the company’s strong operating efficiency.

AI technologies and related products were the primary growth drivers:

- Google’s Search business delivered more than 11% growth in advertising revenue.

- YouTube ad revenue rose by approximately 13%.

- Google Cloud posted an outstanding 32% increase in revenue.

Additional growth catalysts included AI‑powered products, such as AI Overviews, AI Mode, and the Gemini chatbot, all of which were actively integrated into the Google ecosystem. According to company data, AI Overviews were used by more than 2 billion users per month at the time, AI Mode had reached 100 million users in the US and India, and Gemini had 450 million active users.

In its forward guidance, Alphabet announced an increase in capital expenditure for 2025 from 75 billion USD to 85 billion USD. The funds were allocated to expanding data centres, developing cloud infrastructure, and scaling AI platforms – highlighting the seriousness of Alphabet’s strategy in its pursuit of AI leadership.

Despite the strong results, several weaknesses emerged in the report:

- The sharp rise in capital expenditure raised concerns over investment returns

- Operating losses in the Other Bets segment reached USD 1.25 billion, widening from the previous year.

- Questions arose about the viability of investments in areas such as Waymo.

- Regulatory risks have intensified, particularly with ongoing antitrust litigation in the US.

Following the earnings release, Alphabet shares opened 3.4% higher but gave up nearly all gains by the close. The increase in capital spending and continued losses from non-core projects led investors to question the sustainability of current growth rates and capital efficiency. Lingering regulatory risks further pressured sentiment, ultimately offsetting the initial optimism.

Alphabet Inc. Q3 2025 earnings results

On 29 October, Alphabet published its Q3 2025 results for the quarter ended 30 September. The key figures, compared with the same period in 2024, are as follows:

- Revenue: 102.35 billion USD (+16%)

- Net income: 34.98 billion USD (+33%)

- Earnings per share: 2.87 USD (+35%)

- Costs and expenses: 71.12 billion USD (+19%)

- Operating income: 34.69 billion USD (+22%)

- Operating margin: 31% (–100 bps)

Revenue by segment:

- Google Services: 87.05 billion USD (+14%)

- Google advertising: 71.18 billion USD (+13%)

- Google Search & other: 56.57 billion USD (+15%)

- YouTube ads: 10.26 billion USD (+15%)

- Google Network: 7.35 billion USD (–3%)

- Google subscriptions, platforms, and devices: 12.87 billion USD (+21%)

- Google Cloud: 15.16 billion USD (+34%)

- Other Bets: 0.34 billion USD (–11%)

Alphabet’s Q3 2025 report was exceptionally strong, far exceeding analyst expectations. Revenue reached 102.3 billion USD (+16% y/y) – the first time in the company’s history that quarterly revenue has surpassed 100 billion USD, compared with market forecasts of around that level.

Excluding a one-off fine from the European Commission, operating profit came to approximately 34.7 billion USD (+22% y/y), while the operating margin rose to 33.9% from 32.3% a year earlier. Adjusted earnings per share (non-GAAP EPS) were estimated at 3.10 USD, well above the consensus forecast of about 2.26 USD. In other words, the company outperformed expectations on both revenue and profit.

Growth was evident across all business areas. The core Google Services division generated 87.1 billion USD (+14%), including Search – 56.6 billion USD (+15%), YouTube Ads – 10.3 billion USD (+15%), and subscriptions, platforms, and devices – 12.9 billion USD (+21%). The Cloud segment expanded by 34% to 15.2 billion USD, with a backlog of 155 billion USD, which confirms sustained demand for AI infrastructure.

During the earnings call, management highlighted the success of its full-stack AI strategy, spanning proprietary TPU and Axion chips as well as models and products. The company emphasised strong demand for AI-driven solutions across Search, YouTube, and Cloud, describing the quarter as highly successful, with double-digit growth in all key areas.

While Alphabet did not provide detailed revenue or profit guidance for upcoming periods, it raised its full-year capital expenditure outlook to 91–93 billion USD (from 85 billion USD previously). It warned that CapEx would increase further in 2026 due to continued investment in data centres, energy, and AI infrastructure. This indicates that Alphabet anticipates sustained demand for its cloud and AI services over the coming years.

Alphabet Inc. Q4 2025 earnings results

On 4 February, Alphabet published its Q4 2025 results for the period ended 31 December. Below are the key figures compared with the same period in 2024:

- Revenue: 113.83 billion USD (+18%)

- Net income: 34.46 billion USD (+30%)

- Earnings per share: 2.82 USD (+31%)

- Costs and expenses : 77.89 billion USD (+19%)

- Operating income : 35.93 billion USD (+16%)

- Operating margin : 31.6% (–50 basis points)

Revenue by segment:

- Google Services : 95.86 billion USD (+14%)

- Google advertising : 82.28 billion USD (+14%)

- Google Search & other: 63.07 billion USD (+17%)

- YouTube ads: 11.38 billion USD (+9%)

- Google Network: 7.83 billion USD (–2%)

- Google subscriptions, platforms, and devices : 13.58 billion USD (+17%)

- Google Cloud: 17.66 billion USD (+48%)

- Other Bets: 0.37 billion USD (–8%)

Alphabet’s Q4 2025 report was strong in terms of both growth quality and profitability. Quarterly revenue reached 113.83 billion USD (+18% year-on-year), exceeding the consensus estimate of around 111.40 billion USD, while net income rose to 34.46 billion USD (+30% year-on-year). At the EPS level, the company also demonstrated acceleration, with diluted earnings per share of 2.82 USD (+31% year-on-year).

Revenue from Google Search & other increased to 63.07 billion USD (+17% year-on-year), while the overall Google advertising segment rose to 82.28 billion USD. YouTube ads grew by 9% to 11.38 billion USD – moderate yet stable growth, while Google Network declined slightly (7.83 billion USD, –2% year-on-year). Google Cloud was the primary growth driver, increasing revenue by 48% and raising its operating margin to 30.1%.

Alphabet stated that CapEx in 2026 is expected to range between 175–185 billion USD (almost double the 2025 level), overshadowing the positive earnings results. From a business perspective, this signals strong utilisation and demand for computing capacity. However, for the market, it immediately raises questions about free cash flow, depreciation and amortisation, and return on invested capital (ROIC): at this level of capital expenditure, even very strong margins may temporarily appear weaker due to higher D&A and increased energy and equipment requirements.

Financial resilience remains comfortable. At the end of 2025, the company held approximately 126.84 billion USD in cash and marketable securities, meaning Alphabet can finance its investment cycle without liquidity stress. However, it is notable that debt increased significantly (long-term debt of 46.55 billion USD), and in November 2025, the company raised approximately 24.80 billion USD through the issuance of unsecured notes. This suggests that management is already optimising the capital structure in response to the growing capital intensity of the AI race.

Analysis of key valuation multiples for Alphabet Inc.

Below are Alphabet’s key valuation multiples based on Q4 FY 2025 results, calculated using a share price of 302 USD.

| Multiple | What it indicates | Value | Commentary |

|---|---|---|---|

| P/E (TTM) | The price of 1 USD of earnings over the past 12 months | 28.0 | ⬤ Good.

The multiple is appropriate for a tech giant with 30% profit growth. It is lower than many competitors within the Magnificent Seven. |

| P/S (TTM) | The price of 1 USD of annual revenue | 9.1 | ⬤ Moderate. The value is above the historical average (typically 6–7x), indicating that the market is pricing in elevated expectations for AI-driven revenue. |

| EV/Sales (TTM) | Enterprise value to revenue, including debt | 9.2 | ⬤ Moderate. This confirms a premium on the price investors are willing to pay for every dollar of sales in the context of market dominance. |

| P/FCF (TTM) | The price of 1 USD of free cash flow | 49.8 | ⬤ Overvalued. The multiple is heavily inflated due to the reduction in free cash flow (FCF). |

| FCF Yield (TTM) | Free cash flow yield for shareholders | 2.0% | ⬤ Low FCF yield.

This indicates that the company is currently spending almost all its earnings on infrastructure development. |

| EV/EBITDA (TTM) | Enterprise value to EBITDA | 24.6 | ⬤ Stable. The operating income multiple looks resilient, though it is at the upper end of the historical range. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 28.7 | ⬤ Moderate. This multiple confirms that the market places a high value on the company’s operating efficiency. |

| P/B | Price to book value | 8.8 | ⬤ Standard for the sector.

For the IT sector, with a high proportion of intangible assets, this is a typical value. |

| Forward P/E | Forward price-to-earnings (P/E) ratio | 24.5 | ⬤ Good. The expected reduction in the multiple with profit growth in 2026 makes the shares attractive for long-term investors. |

| Net Debt/EBITDA | Debt load relative to EBITDA | 0.31 | ⬤ Ideal leverage state.

The company still has vast liquidity, significantly exceeding its debts. |

| Interest Coverage (TTM) | Operating profit to interest expense ratio | 50 | ⬤ Minimal interest expenses. Alphabet practically incurs no noticeable interest costs. |

Valuation multiples analysis for Alphabet Inc. – conclusion

Alphabet’s financial position at the end of 2025 can be characterised as a period of aggressive investment.

On the one hand, the company’s operating profitability and balance sheet strength remain very solid. The market continues to show confidence in the success of Gemini and cloud technologies, which are supporting the stock at elevated levels.

On the other hand, the red zone in free cash flow metrics is a direct result of management’s strategic decision to double capital expenditure to 175–185 billion USD in 2026. Alphabet is deliberately sacrificing current cash flow to build AI infrastructure and avoid falling behind Microsoft and Meta in the technological arms race.

The shares do not appear inexpensive, but the pace of growth justifies their valuation. The key risk in 2026 is that if these substantial investments fail to generate proportional revenue growth in the Cloud and Search segments, this could trigger a downward revision of valuation multiples. At present, Alphabet remains a financially resilient growth company operating under an elevated investment burden.

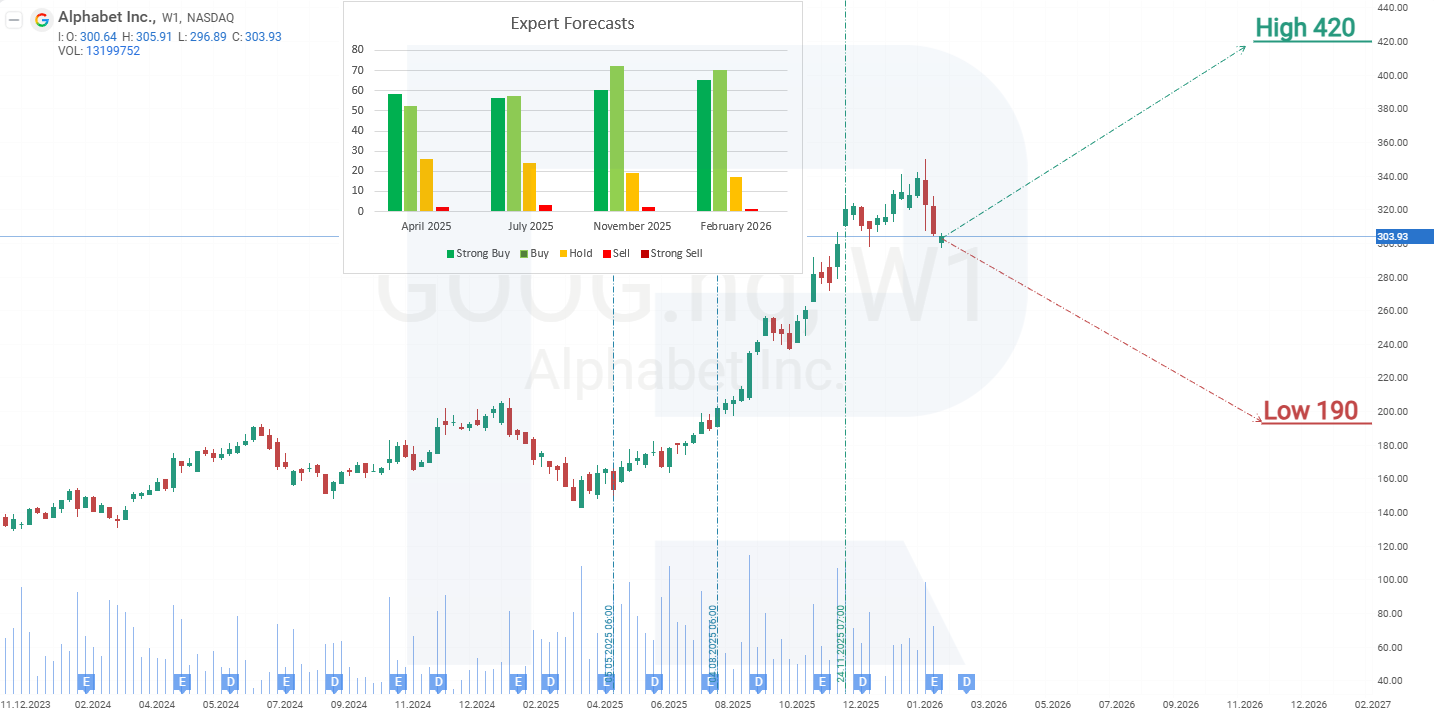

Expert forecasts for Alphabet Inc. stock

- Barchart: 46 out of 55 analysts rated Alphabet shares as Strong Buy, 3 as Moderate Buy, and 6 as Hold. The upper price target is 420 USD, and the lower bound is 220 USD.

- MarketBeat: 36 out of 41 specialists assigned a Buy rating to the shares, 4 recommended Hold, and 1 recommended Sell. The upper price target is 420 USD, and the lower bound is 210 USD.

- TipRanks: 12 out of 13 analysts assigned a Buy rating to the shares, and 1 recommended Hold. The upper price target is 420 USD, and the lower bound is 348 USD.

- Stock Analysis: 19 out of 44 experts rated the shares as Strong Buy, 19 as Buy, and 6 as Hold. The upper price target is 420 USD, and the lower bound is 190 USD.

Alphabet Inc. stock price forecast for 2026

On the weekly chart, Alphabet shares reached the 350 USD resistance level in February 2026 and then moved lower. From April 2025 to February 2026, GOOG shares rose by 145% without significant corrections, increasing the likelihood of a price decline following a rejection at the 350 USD resistance level. The current decline can be viewed as a technical correction within the ongoing long-term uptrend. Based on the current performance of Alphabet Inc. shares, the potential price movements for 2026 are as follows:

The base-case forecast for Alphabet stock suggests the shares are likely to decline further towards the support level at 260 USD, where the correction is expected to end, and the long-term uptrend should resume. The first target for recovery would be the historical high, around 350 USD. If this level is breached, the next target could be 480 USD, calculated using Fibonacci levels.

The alternative forecast for Alphabet shares suggests that a break below the 260 USD support level could see GOOG shares fall to the 205 USD support level, where a recovery towards 350 USD is likely. This scenario could unfold if the broader US stock market outlook worsens, leading to a large-scale correction in the technology sector. In such an environment of reduced risk appetite, investors may revise their earnings growth expectations needed to justify the current valuation multiples.

Alphabet Inc. challenges NVIDIA’s dominance in the AI chip market

NVIDIA may not hold a formal monopoly, but it effectively dominates the market for AI data centre hardware. Alphabet is now seeking to disrupt this advantage by building its own ecosystem.

Alphabet has been developing its Tensor Processing Units (TPUs) for many years, deploying them across its core services – Search, YouTube, Maps, and its Gemini model. The latest generation, TPU v5p, can be combined into clusters of up to 8,960 chips and delivers substantial improvements in performance and energy efficiency compared with previous versions. This makes it a direct competitor to NVIDIA’s GPUs, but with full integration into the Google Cloud and Vertex AI ecosystems.

Previously, TPUs were used mainly within Google or offered to clients through cloud rental. However, the company is currently taking them to the external market – entering a space that NVIDIA had largely dominated until now.

A key part of Alphabet’s strategy is the creation of a complete technological stack – from hardware to software. In 2024, Google introduced its own server processor, Axion, based on Arm architecture, which the company claims outperforms rivals in both performance and energy efficiency. In combination with TPUs, networking solutions, and management systems such as AI Hypercomputer, Vertex AI, and TPU Command Center, this enables major clients to build fully functional AI clusters without relying on NVIDIA’s products.

Alphabet has been actively demonstrating the capabilities of its technologies in practice – the new Gemini 3 model is trained and operates entirely on TPUs. According to several reviews, its performance and quality are comparable to, or even exceed, the latest versions of ChatGPT, making a persuasive case for potential enterprise clients.

Several recent developments have directly weakened NVIDIA’s position. On 27 August 2025, Meta signed a six-year cloud contract worth around 10 billion USD with Google Cloud to support large-scale AI projects, in which TPU chips and the Vertex AI platform play a central role. This is no longer a pilot initiative but a major commercial deal with a global client that will now use Alphabet’s infrastructure instead of NVIDIA GPUs provided by other vendors.

On 21 October 2025, TrendForce confirmed that Axion server processors are being manufactured using TSMC’s advanced 3-nanometre process technology. This indicates that Alphabet is developing not experimental chips but a scalable, high-performance solution for its data centres – capable of competing directly with NVIDIA’s offerings.

In November 2025, it was reported that Meta entered negotiations to purchase TPUs from Alphabet in a multi-billion-dollar deal. The company plans to rent TPUs through Google Cloud from 2026 and begin installing them in its own data centres from 2027. The total volume of these potential deals is estimated at several billion dollars and, according to Google Cloud’s internal assessments, could divert up to 10% of NVIDIA’s annual AI chip revenue.

Industry reports note that the market is gradually reassessing the structure of AI-related investments. As Alphabet achieves progress in chip design, cloud infrastructure, and the rollout of its Gemini model, investor sentiment is shifting, with NVIDIA no longer appearing to be the only clear beneficiary of the AI boom. Increasingly, Alphabet is viewed as a more balanced and diversified play on AI infrastructure and ecosystem growth, while NVIDIA’s shares are undergoing a correction following a prolonged rally.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.