Alibaba – increasing investment in AI and cloud: BABA price targets at 145 and 180 USD in 2026

Alibaba grew revenue and accelerated its cloud business, but profit was pressured due to substantial investment in AI and quick commerce. The base forecast for 2026 anticipates a rise in BABA shares to 145 USD, with potential for further upside to 180 USD if the stock breaks above resistance.

Alibaba Group Holding Limited (NYSE: BABA) reported revenue growth and strong progress in its cloud and AI segments in the December 2025 quarter. However, profitability declined sharply due to rising expenses and investments. The report confirmed that the company is prioritising the expansion of quick commerce and AI infrastructure, even at the expense of short-term margin pressure.

The December 2025 quarter was mixed for Alibaba. Revenue increased only 2% year-on-year to 40.73 billion USD, GAAP net income fell 66% to 2.24 billion USD, and non-GAAP net income declined 67% to 2.39 billion USD. As a result, both revenue and net income came in below analyst forecasts.

Once again, the cloud and AI-related segments performed best. The Cloud Intelligence Group grew revenue by 36% year-on-year. The company highlighted that revenue from AI-related products has posted triple-digit growth for the tenth straight quarter. Domestic e-commerce in China rose 6% year-on-year, the international segment increased by 4% year-on-year, and quick commerce grew 56% year-on-year.

Although the company did not provide a precise quarterly revenue or earnings forecast, management clearly outlined its future priorities. Alibaba stated that in the coming quarters, it will continue to improve unit economics in Taobao Quick Commerce, aiming to scale this business to 1 trillion yuan and reach profitability by the 2029 financial year. At the same time, management is making a significantly larger strategic bet on AI and cloud: CEO Eddie Wu said the company’s five-year target is to exceed 100 billion USD in external revenue from cloud and AI.

This article examines Alibaba Group Holding Limited, outlining its key revenue sources, providing a fundamental analysis of Alibaba Group (BABA), and presenting a technical analysis of BABA shares, which forms the basis for the Alibaba Group stock price forecast for 2026.

About Alibaba Group Holding Limited

Alibaba Group Holding Limited is the largest Chinese technology company. Founded in 1999 in Hangzhou by Jack Ma (also known as Ma Yun) and his team, the company operates in e-commerce, cloud computing, financial technologies, logistics, and the media and entertainment sectors. Its platforms (AliExpress, Taobao, and Tmall) connect millions of buyers and sellers worldwide. Alibaba is also actively advancing Artificial Intelligence (AI) and innovative technologies, playing a pivotal role in the global digital economy.

Alibaba’s initial public offering (IPO), which raised USD 25.0 billion, took place on 19 September 2014 on the New York Stock Exchange under the ticker symbol BABA. At the time, it was the largest IPO in history.

Alibaba Group Holding Limited’s main financial flows

Alibaba Group’s revenue is generated across several core segments:

- Alibaba China E-commerce Group: the company’s primary domestic e-commerce business in China. Revenue is derived from Taobao and Tmall, quick commerce services via Taobao Instant Commerce and Ele.me, the Fliggy platform, Chinese wholesale operations, as well as customer management revenue, direct sales, logistics, and value-added services. This segment remains the group’s main source of revenue.

- Alibaba International Digital Commerce Group: international digital commerce. Revenue comes from international retail and wholesale operations, including AliExpress and other overseas channels, as well as cross-border value-added services.

- Cloud Intelligence Group: Alibaba Cloud’s computing and AI products. Revenue is generated from public cloud services, data storage and processing, computing capacity, enterprise cloud services, and AI-related solutions.

- All others: this category includes Freshippo, Cainiao, Alibaba Health, Hujing Digital Media and Entertainment Group, Amap, Qwen Consumer Business Group, Lingxi Games, DingTalk, and other businesses. Most of the revenue in this segment is generated from direct sales and logistics services.

Alibaba Group Holding Limited September 2024 financial results

On 15 November 2024, Alibaba Group Holding Limited released its financial results for the quarter ended 30 September 2024. The key figures from the report are outlined below:

- Revenue: 33.70 billion USD (+5%)

- Net income: 6.20 billion USD (+63%)

- Earnings per share: 2.59 USD (+69%)

Revenue by segment:

- Taobao and Tmall Group: 14.10 billion USD (+1%)

- Cloud Intelligence Group: 4.22 billion USD (+7%)

- International Digital Commerce Group: 4.51 billion USD (+29%)

- Cainiao Smart Logistics Network: 3.51 billion USD (+8%)

- Local Services Group: 2.52 billion USD (+14%)

- Digital Media and Entertainment Group: 0.81 billion USD (–1%)

- All others: 7.43 billion USD (+9%)

In comments on the results, CEO Eddie Wu highlighted robust revenue growth from cloud solutions and AI products. He also cited strategic agreements with key partners aimed at improving payment and logistics services on the Taobao and Tmall platforms.

Alibaba Group’s net profit for the September 2024 quarter rose by an impressive 63% year-on-year, primarily driven by a positive revaluation of the company’s investments.

The e-commerce segment, which includes the Taobao and Tmall platforms, delivered solid growth supported by double-digit increases in order volumes and revenue from customer services, further strengthening Alibaba’s position in the domestic market. Revenue from Alibaba Cloud increased by 7%, primarily driven by triple-digit growth in income from AI-related products. Cost optimisation and improved operational efficiency across several business units also supported profitability, allowing the company to manage expenses effectively amid ongoing economic uncertainty.

However, despite the rise in net profit, non-GAAP net income, which excludes one-off items such as investment revaluations, declined by 9% to 5.20 billion USD. The company attributed this decline to substantial investments in Alibaba Cloud and refunds to merchants following the cancellation of annual service fees.

Alibaba also rewarded its shareholders with a share buyback worth 4.1 billion USD.

Alibaba Group Holding Limited December 2024 financial results

On 20 February 2025, Alibaba Group Holding Limited published its financial results for the quarter ended 31 December 2024. The key highlights are outlined below:

- Revenue: 38.38 billion USD (+8%)

- Net income: 6.36 billion USD (+333%)

- Earnings per share: 2.93 USD (+13%)

Revenue by segment:

- Taobao and Tmall Group: 18.64 billion USD (+5%)

- Cloud Intelligence Group: 4.34 billion USD (+13%)

- International Digital Commerce Group: 5.17 billion USD (+32%)

- Cainiao Smart Logistics Network: 3.86 billion USD (–1%)

- Local Services Group: 2.32 billion USD (+12%)

- Digital Media and Entertainment Group: 0.75 billion USD (+8%)

- All others: 7.27 billion USD (+13%)

CEO Eddie Wu highlighted the company’s significant progress in advancing its user-first strategy and harnessing innovative AI technologies. He emphasised that Alibaba remains committed to making substantial investments in cloud technologies and AI infrastructure to maintain its competitive edge.

In the long term, Alibaba plans to invest 53.00 billion USD in cloud computing and AI over the next three years, aiming to become the world’s leading cloud provider.

Although the company did not provide a specific financial outlook for the next quarter, analysts anticipate continued growth. However, the announcement of the 53.00 billion USD investment has raised concerns among investors, as it could weigh on the company’s net profit.

Alibaba Group Holding Limited March 2025 financial results

On 15 May 2025, Alibaba Group Holding Limited released its financial results for the quarter ended 31 March 2025. The key figures are outlined below:

- Revenue: 32.58 billion USD (+7%)

- Net income: 1.65 billion USD (+1203%)

- Earnings per share: 0.71 USD (+296%)

Revenue by segment:

- Taobao and Tmall Group: 13.96 billion USD (+9%)

- Cloud Intelligence Group: 4.15 billion USD (+18%)

- International Digital Commerce Group: 4.62 billion USD (+22%)

- Cainiao Smart Logistics Network: 2.97 billion USD (–12%)

- Local Services Group: 2.22 billion USD (+10%)

- Digital Media and Entertainment Group: 0.77 billion USD (+12%)

- All others: 7.44 billion USD (+5%)

Alibaba Group Holding’s quarterly report demonstrated steady growth across key areas. The company’s revenue rose 7% compared with the same period last year. The main driver was the Taobao and Tmall e-commerce platforms, which recorded a 9% growth. The international e-commerce segment also showed resilience, rising by 22%, highlighting Alibaba’s ongoing efforts to expand globally.

The Cloud Intelligence Group division remained one of the key contributors to growth, with strong demand for AI-related products playing a crucial role.

However, despite these strong figures, the company’s net income fell short of analysts’ expectations, causing Alibaba’s shares in the US to drop around 7%. Additional pressure came from weakening consumer activity in China and intensifying competition.

Alibaba’s management expressed confidence in achieving a return to double-digit revenue growth in the second half of 2025, driven by continued investment in cloud technology and artificial intelligence. The company’s strategic focus on innovation and digital transformation provides a firm foundation for further expansion.

Alibaba Group Holding Limited June 2025 financial results

On 29 August 2025, Alibaba Group Holding Limited published its financial results for the quarter ended 30 June. Key figures are as follows:

- Revenue: 34.57 billion USD (+2%)

- Net income: 5.92 billion USD (+76%)

- Earnings per share: 2.51 USD (+82%)

Revenue by segment:

- Alibaba China E‑commerce Group: 19.55 billion USD (+10%)

- Alibaba International Digital Commerce Group: 4.85 billion USD (+19%)

- Cloud Intelligence Group: 4.66 billion USD (+26%)

- All others: 8.18 billion USD (–28%)

Against the backdrop of slowing domestic consumer demand and increased investment in strategic priorities, Alibaba delivered mixed results for the June quarter 2025. Total revenue grew by just 2% year-on-year to 247.65 billion CNY (34.57 billion USD), falling slightly short of analysts’ expectations. However, after excluding divested assets Sun Art and Intime, organic growth in core segments was approximately 10%, signalling continued domestic business transformation.

The most positive momentum came from the cloud segment, where revenue increased by 26% year-on-year, driven by rising demand for AI solutions and ongoing investment in proprietary infrastructure. The company is advancing its own large language models under the Qwen brand and continues to develop specialised AI chips, aiming to reduce dependency on suppliers such as NVIDIA. The international segment, including AliExpress, Trendyol, and Cainiao, also delivered strong year-on-year growth of 19%, supported by expansion in key regions and strengthened logistics capabilities.

The domestic e‑commerce segment (China) grew by 10%, although margins came under pressure due to aggressive investment in instant-commerce initiatives. Alibaba faces intense competition from Meituan and JD.com in the rapid delivery space, resulting in higher costs and reduced operational efficiency.

GAAP net income rose 78% to 43.1 billion CNY (6.01 billion USD), largely due to one-off gains from the sale of the Trendyol stake and investment revaluations. Adjusted profit, however, fell 18% to 4.91 billion USD, and EBITDA declined 14%, reflecting a more accurate picture of the company’s underlying operational performance.

No forecasts were provided for revenue, margins, or investment expenditures. However, in the commentary accompanying the report, management emphasised that it continues to actively invest in two strategic focus areas: Consumption and AI + Cloud. CapEx and cash outflows were expected to remain above normal levels over the coming quarters due to investment in cloud and AI infrastructure, after which the effect was projected to normalise as monetisation – primarily in cloud – progresses. Management anticipated further accelerated growth in the cloud business driven by GenAI workloads. In e‑commerce, the focus remained on expanding the user base and order volumes, followed by monetisation. In the international segment, emphasis was placed on strengthening positions in key regions (Europe, the Middle East, and Korea), enhancing efficiency (AliExpress, Trendyol), and further integrating logistics (Cainiao).

Alibaba Group Holding Limited September 2025 financial results

On 29 November 2025, Alibaba Group Holding Limited released its financial results for the quarter ended 30 September. The key figures are as follows:

- Revenue: 34.81 billion USD (+5%)

- Net income: 1.45 billion USD (–72%)

- Earnings per share: 0.61 USD (–71%)

Revenue by segment:

- Alibaba China E-commerce Group: 18.62 billion USD (+16%)

- Alibaba International Digital Commerce Group: 4.89 billion USD (+10%)

- Cloud Intelligence Group: 5.59 billion USD (+34%)

- All others: 8.85 billion USD (–25%)

Alibaba’s September 2025 quarter report was mixed: while revenue rose more strongly than expected, profit dropped sharply. The company generated 34.8 billion USD (+5% y/y, or +15% excluding the divested Sun Art and Intime assets), slightly above analyst forecasts. Growth was driven by the cloud business (+34% y/y) and international e-commerce, including quick-commerce services.

However, profit declined steeply: adjusted net income fell to 1.45 billion USD (–72% y/y), while earnings per share came in at 0.61 USD, around 20% below expectations. The main reasons were heavy marketing spending, discounts, the end of quick commerce, and increased investment in AI and cloud infrastructure. Adjusted EBITA fell by 80% to 1.27 billion USD, and free cash flow turned negative (–3.1 billion USD) due to higher capital expenditure and working capital requirements.

Management expected that spending on quick commerce had already peaked: in the next quarter, subsidy and marketing costs would decline, while order economics would improve. The company planned to grow its quick-commerce turnover to approximately 138 billion USD over three years and invest more than 52 billion USD in cloud and AI development.

Overall, while the report is characterised as strong in terms of growth, it was weak in profitability: the business was expanding rapidly, with cloud revenue growing faster than expected. However, profit and cash flow remained under pressure due to the heavy investment burden. In the coming quarters, Alibaba, in effect, was prioritising market share and future leadership in AI and e-commerce, sacrificing short-term returns.

Alibaba Group Holding Limited December 2025 financial results

On 19 March 2026, Alibaba Group Holding Limited released its financial results for the quarter ended 31 December 2025. The key figures are as follows:

- Revenue: 40.73 billion USD (+2%)

- Net income: 2.24 billion USD (–66%)

- Earnings per share: 0.85 USD (–67%)

Revenue by segment:

- Alibaba China E-commerce Group: 22.79 billion USD (+6%)

- Alibaba International Digital Commerce Group: 5.61 billion USD (+4%) #. Cloud Intelligence Group: 6.19 billion USD (+36%)

- All others: 9.63 billion USD (–25%)

Alibaba’s December 2025 quarter was weak in terms of current profitability. Revenue rose 2% year-on-year, but the result fell short of market expectations. Net income declined 67% year-on-year, while non-GAAP earnings per ADS were 1.01 USD, also significantly below consensus. The main positive highlight once again was the cloud segment, where Cloud Intelligence Group revenue increased 36% year-on-year.

The main issue during the quarter was substantial pressure on margins and cash flow. Operating profit fell 74% year-on-year, adjusted EBITA declined 57%, and the margin contracted from 20% to 8%. Free cash flow remained positive but fell 71% to 1.62 billion USD, while operating cash flow declined by 49%. The primary reasons for these results were aggressive investment in quick commerce, enhancements to the user experience, and technological infrastructure. This is clearly reflected in the cost structure, with sales and marketing expenses rising to 25.3% of revenue, compared with 15.2% a year earlier.

At the same time, there were positive signals. Alibaba China E-commerce Group grew by 6%, international digital commerce increased by 4%, and quick commerce surged by 56% to 2.98 billion USD. Management also highlighted improved order economics in quick commerce, with rising average order values, stronger customer retention, and greater logistics efficiency.

Alibaba did not provide quantitative guidance for the next quarter, instead offering qualitative guidance. Management expects continued growth in the cloud business and AI, as well as gradual improvement in the economics of quick commerce in the coming quarters.

Analysis of key valuation multiples for Alibaba Group Holding Limited

Below are Alibaba Group Holding Limited’s key valuation multiples based on the December 2025 quarter results, calculated using a share price of 126 USD.

| Multiple | What it indicates | Value | Comment |

|---|---|---|---|

| P/E (TTM) | The price of 1 USD of earnings over the past 12 months | 21.34 | ⬤ Valuation is moderate. |

| P/S (TTM) | The price of 1 USD of annual revenue | 1.95 | ⬤ On a revenue basis, the valuation appears reasonable. |

| EV/Sales (TTM) | Enterprise value to revenue, including debt | 1.66 | ⬤ The substantial net cash position makes the stock look relatively attractive. |

| P/FCF (TTM) | The price of 1 USD of free cash flow | n/a | ⬤ Trailing FCF is negative. |

| FCF Yield (TTM) | Free cash flow yield for shareholders | n/a | ⬤ Trailing FCF remains negative. |

| EV/EBITDA (TTM) | Enterprise value to EBITDA | 12.13 | ⬤ Overall, the valuation is fair. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 21.18 | ⬤ On current EBIT levels, the stock already appears somewhat expensive. |

| P/B | Price to book value | 1.91 | ⬤ Acceptable valuation for a company with a strong balance sheet. |

| Forward P/E | Forward price-to-earnings (P/E) ratio | 15.65 | ⬤ Forward P/E is below the current P/E, indicating that the market expects a recovery in earnings. |

| Net Debt/EBITDA | Debt load relative to EBITDA | –2.14 | ⬤ Very strong balance sheet, with the company holding net cash. |

| Interest Coverage (TTM) | Operating profit to interest expense ratio | 7.91 | ⬤ Interest expenses are comfortably covered. |

Alibaba currently appears to be an attractive buying opportunity. The company has a very strong balance sheet, a substantial cash buffer, and, overall, a moderate valuation relative to revenue, providing solid financial support for the business. This means that Alibaba has a margin of safety even during periods when profits and cash flow remain under pressure.

On the other hand, current free cash flow appears weak, and the stock no longer looks inexpensive based on operating income. Therefore, buying Alibaba now is not a bet on a very low valuation, but rather a bet that the company can gradually restore profitability, improve margins, and generate stronger cash flow in the coming quarters.

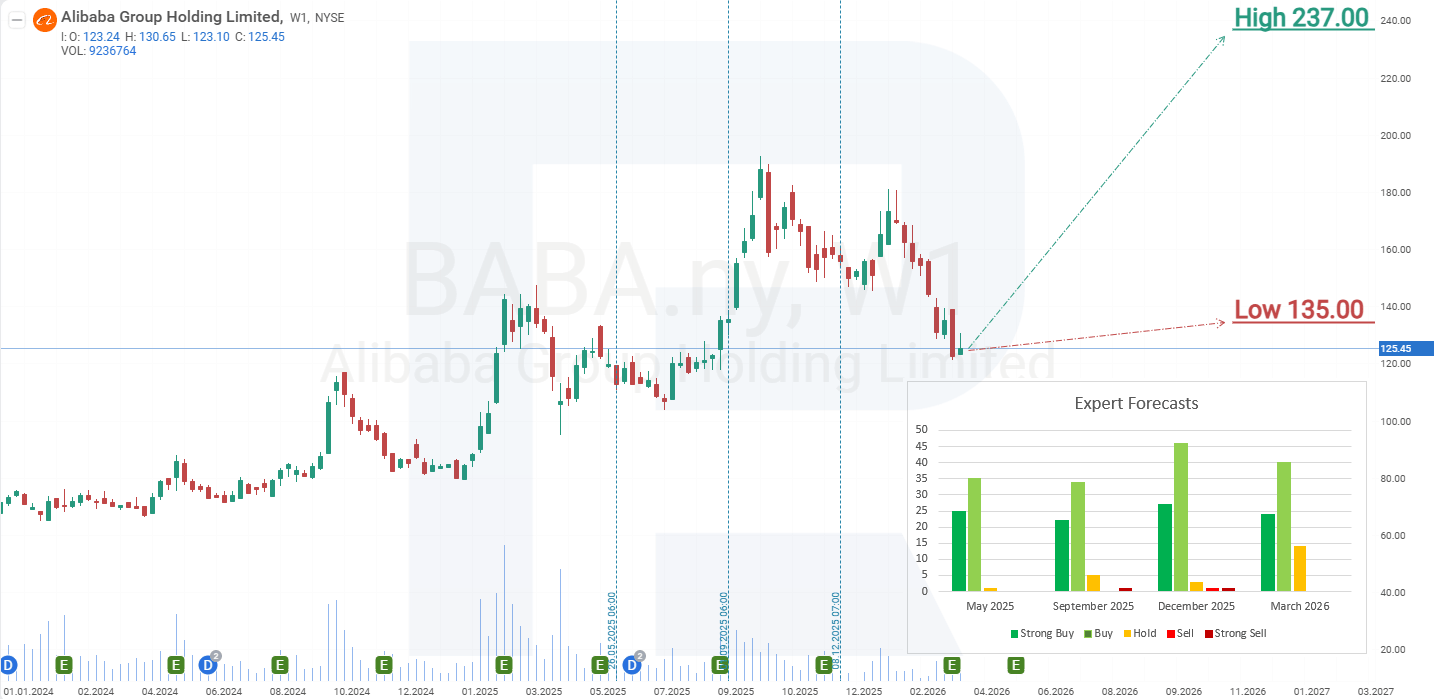

Expert forecasts for Alibaba Group Holding Limited’s stock for 2026

- Barchart: 19 out of 25 analysts rated Alibaba Group shares as Strong Buy, 1 as Moderate Buy, and 5 as Hold. The upper price target is 212 USD, and the lower bound is 135 USD.

- MarketBeat: 16 out of 22 analysts assigned a Buy rating, and 6 recommended Hold. The upper price target is 237 USD, and the lower bound is 135 USD.

- TipRanks: 16 out of 18 analysts rated the shares as Buy, and 2 as Hold. The upper price target is 215 USD, and the lower bound is 135 USD.

- Stock Analysis: 5 out of 13 experts rated Alibaba Group shares as Strong Buy, 7 as Buy, and 1 as Hold. The upper price target is 225 USD, and the lower bound is 135 USD.

Alibaba Group Holding Limited stock price forecast for 2026

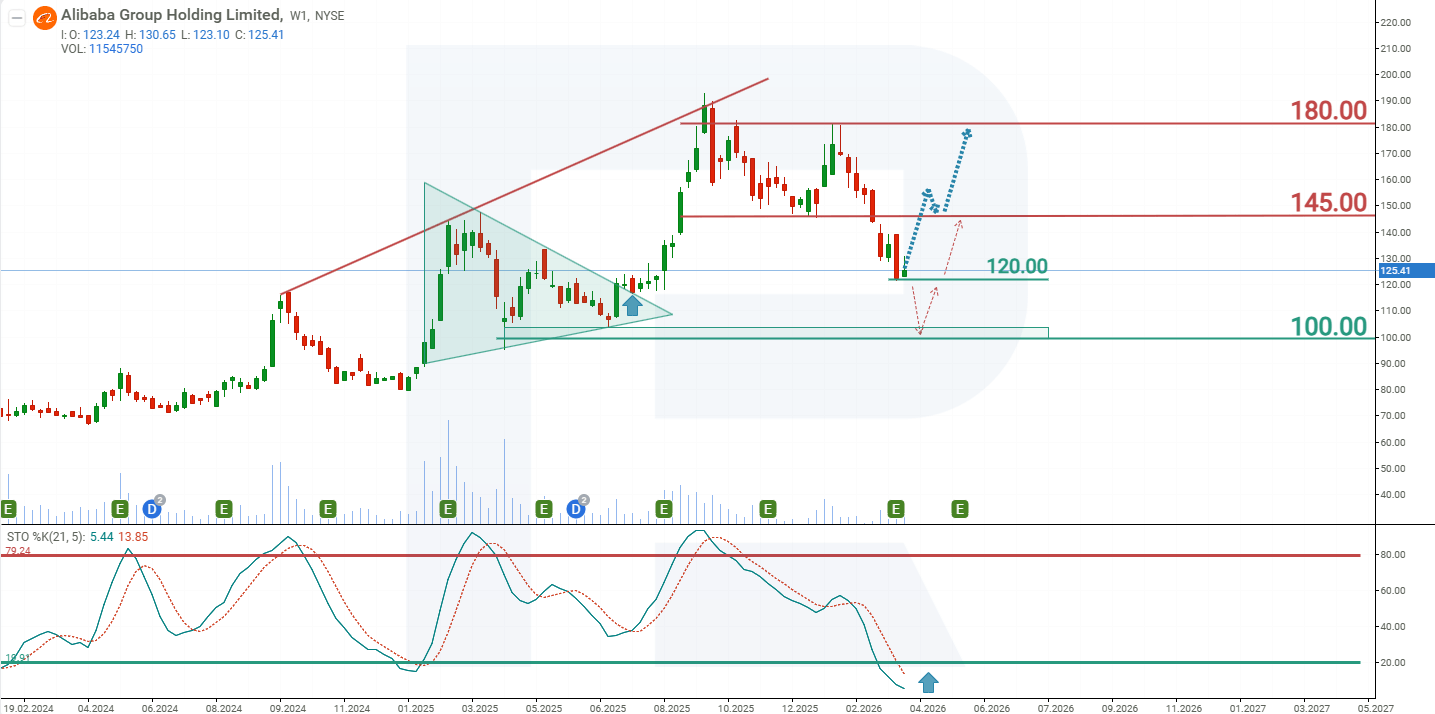

In October 2022, Alibaba shares reached a local low of 55 USD. This marked the end of a prolonged decline that had begun in October 2020, following intensified regulatory pressure in China. Over this period, BABA fell by 82%, making it one of the weakest performers among major Chinese technology companies.

The situation began to improve in January 2024. The market responded positively to news that Jack Ma had purchased 200 million USD worth of Alibaba shares. Additional support came from a sharp increase in the company’s share buyback program. During the 2024 financial year, Alibaba spent 12.5 billion USD on buybacks, making it the leader among Chinese companies in terms of shares repurchased.

Against this backdrop, Alibaba shares moved into an uptrend and, by September 2025, had risen to 192 USD, representing a gain of nearly 200% from the 2022 lows. Following this strong advance, the stock entered a correction phase, which remains ongoing. However, the Stochastic indicator is already in oversold territory, suggesting that the correction may be nearing completion and that a resumption of the share price uptrend is possible. Based on the current price dynamics of Alibaba Group Holding Limited shares, the potential price scenarios for 2026 are as follows:

The primary forecast for Alibaba Group Holding Limited shares anticipates a rise in BABA towards the next resistance at 145 USD. A break above this level could act as a catalyst for further upside, potentially driving the share price to the subsequent resistance at 180 USD.

The alternative forecast for Alibaba stock assumes a break below support at 120 USD. In this scenario, the correction could deepen to 100 USD, where investor interest in Alibaba shares is likely to strengthen, potentially creating conditions for a rebound towards 145 USD.

Risks of investing in Alibaba Group Holding Limited stock

Investing in Alibaba Group may involve several risks, which could be particularly significant amid China’s economic measures and policies. The main risks are listed below:

- Connection with the economic stimulus: if the Chinese government cancels or inadequately stimulates the economy, this could negatively impact Alibaba’s shares.

- Global economic conditions: like many large tech companies, Alibaba relies heavily on global markets. For example, economic instability, trade wars, or a decline in global demand could exert pressure on the company’s earnings.

- Trade risks: like other Chinese companies, Alibaba faces the risk of trade sanctions from the US. In particular, restrictions on Chinese companies’ access to Western markets, including US-based platforms, could hinder business expansion and reduce profitability.

- Regulatory and political risks: like other Chinese tech companies, Alibaba operates under strict control by Chinese authorities. In recent years, the Chinese government has tightened regulations in the technology and internet sectors, leading to a significant decline in Alibaba’s market capitalisation. The company is also actively expanding its financial services through its subsidiary, Ant Group, which offers lending, mobile payments, and other services. However, the Chinese government has already imposed restrictions on Ant Group’s growth, negatively affecting the company’s stock. At this stage, the realisation of regulatory risks is unlikely, as the Chinese government is implementing measures to stimulate the economy and is unlikely to complicate business operations in the current climate.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.