Ford shares: targets at 16.50 and 20 USD amid EBIT guidance of around 10 billion USD

Ford’s Q4 2025 report presented a mixed performance: revenue was strong at 45.9 billion USD, but Adjusted EPS was just 0.13 USD, and the company recorded a significant GAAP loss due to impairments related to its EV assets. However, management issued optimistic guidance for 2026, forecasting EBIT of up to 10 billion USD and sustainable free cash flow of up to 6 billion USD.

In Q4 2025, Ford Motor Company (NYSE: F) generated revenue of 45.9 billion USD (-5% year-on-year) and earnings per share of 0.13 USD. Revenue exceeded expectations, but earnings per share came in below forecasts. Under GAAP standards, the company reported a net loss of 11.1 billion USD due to one-off impairments totalling 15.5 billion USD, primarily related to a reassessment of its electric vehicle investments and the cancellation of certain programs.

The main profit driver remains Ford Pro: 14.9 billion USD in revenue and 1.23 billion USD in EBIT for the quarter. The Model e segment remains loss-making, with 1.3 billion USD in revenue and an EBIT loss of 1.22 billion USD. The traditional Ford Blue business generated 26.2 billion USD in revenue, while operating profit declined to 0.7 billion USD, indicating margin pressure.

For 2026, the company provided a more constructive outlook: adjusted EBIT of 8–10 billion USD and free cash flow of 5–6 billion USD. However, losses in the electric vehicle and software segments are still expected at 4–4.5 billion USD, meaning the strategy relies on Ford Pro’s profitability and strict cost control while the EV business undergoes restructuring.

This article examines Ford Motor Company’s business model and revenue structure, presents its quarterly results, and provides a fundamental analysis of Ford’s stock under the ticker F. It also outlines expert forecasts for Ford shares in 2026 and reviews recent Ford share price dynamics, forming the basis for the Ford Motor Company stock forecast for 2026.

About Ford Motor Company

Ford Motor Company was founded by Henry Ford in 1903 in the US. The company’s primary business activities involve designing, manufacturing, and marketing a wide range of vehicles, including passenger cars, trucks, SUVs, and commercial vehicles. Additionally, Ford is actively involved in the financial sector through its subsidiary, Ford Motor Credit Company, which offers car buyers leasing, lending, and other financial products.

The IPO took place in 1956, making Ford the first automaker to be listed on the New York Stock Exchange under the ticker symbol “F.” This opened new opportunities for investors and supported the company’s continued growth and development.

Today, Ford continues to innovate in the automotive industry, focusing on electric vehicles and autonomous technologies while improving the environmental performance of its products in response to evolving market demands and existing trends.

Ford Motor Company’s main revenue streams

Ford divides its operations into key divisions and publishes financial results for each, except Ford Next, which has not yet generated income. Below are Ford’s main divisions and business areas:

- Ford Blue: traditional production of internal combustion engine vehicles (ICE) and hybrid vehicles. This represents the core of Ford’s business and includes the production and sale of classic models such as the Ford F-150, Ford Explorer, and Mustang.

- Ford Pro: production of commercial vehicles and provision of related services. This division serves clients who use vehicles for business purposes.

- Ford E: development and sale of electric vehicles (EVs) and innovative technologies. This department oversees models such as the Ford Mustang Mach-E and F-150 Lightning, as well as the development and promotion of new electric vehicle platforms.

- Ford Next: developing new business models and innovative solutions beyond traditional automobile production. This unit is responsible for the research and development of autonomous driving technologies, new mobility formats, and other promising projects that may lay the foundation for the company’s further growth.

- Ford Credit: this is the company’s financial division that offers loan facilities to retail vehicle buyers and company dealers. The division’s operations include leasing, vehicle financing, and dealer financing for inventory replenishment.

Ford Motor Company Q2 2024 results

Ford released its Q2 2024 financial results on 4 July 2024. Below are the report’s financial indicators:

- Revenue: 47.8 billion USD (+6%)

- Net profit: 1.8 billion USD (–6%)

- Earnings per share: 0.47 USD (–35%)

- Ford Blue revenue: 26.7 billion USD (+7%)

- EBIT: 1.2 billion USD (–48%)

- Ford Pro revenue: 17.0 billion USD (+9%)

- EBIT: 2.6 billion USD (+8%)

- Ford Model e revenue: 1.1 billion USD (–37%)

- EBIT: -1.1 billion USD (unchanged)

- Ford Credit revenue: 3.0 billion USD (+20%)

- EBIT: 0.3 billion USD (–25%)

- Total vehicle sales: 536,050 pcs (+0.8%)

- Electric vehicles: 23,957 pcs (+61%)

- Hybrids: 53,822 pcs (+55%)

- ICE: 458,271 pcs (–0.5%)

The report shows that revenue growth was primarily driven by the Ford Pro division, which recorded a 9% increase and achieved the highest margins among all business units. Ford ranked second after Tesla (NASDAQ: TSLA) in terms of electric vehicle sales, ahead of GM with 21,930 vehicles sold. However, unlike Tesla, Ford’s electric cars are not yet profitable, as reflected by the Ford E division’s loss of 1.1 billion USD. Consequently, Ford’s management decided to cut production of the F-150 Lightning pickup truck and postpone 12.0 billion USD in planned investments for electric vehicle development. Instead, the company is focusing on compact electric vehicles with higher margins. In this segment, Ford aims to compete with Tesla and the Chinese company BYD, which produces low-cost electric cars.

Ford Motor Company Q3 2024 results

Ford released its financial Q3 2024 results on 29 October 2024. Below are the report’s key financial indicators:

- Revenue: 46.2 billion USD (+5%)

- Net profit: 0.9 billion USD (–25%)

- Earnings per share: 0.47 USD (–26%)

- Ford Blue revenue: 26.2 billion USD (+3%)

- EBIT: 1.6 billion USD (–5%)

- Ford Pro revenue: 15.7 billion USD (+13%)

- EBIT: 1.8 billion USD (+9%)

- Ford E revenue: 1.2 billion USD (–33%)

- EBIT: –1.2 billion USD (compared to a loss of 1.3 billion USD a year earlier)

- Ford Credit revenue: 3.1 billion USD (+19%)

- EBIT: 0.5 billion USD (+25%)

- Total vehicle sales: 504,039 pcs (+1%)

- Electric vehicles: 23,509 pcs (+12%)

- Hybrids: 48,101 pcs (+38%)

- ICE: 432,429 pcs (–3%)

The report data shows that the company continues to face challenges with margins for electric vehicle. Despite growth in EV sales, this segment remains unprofitable and requires ongoing investment, which has negatively affected net income, resulting in a 25% decline. However, the Ford Blue and Pro segments, which focus on internal combustion engine (ICE) cars and serve the commercial sector with after-sales service, are helping to mitigate these challenges. Ford Credit is another crucial division that supports the company during difficult times.

Ford Motor Company Q4 2024 results

Ford delivered its Q4 2024 financial results on 5 February 2025. Below are the report’s financial indicators:

- Revenue: 48.2 billion USD (+5%)

- Net profit: 1.8 billion USD (versus a loss of 0.5 billion USD a year earlier)

- Earnings per share: 0.45 USD (versus a loss of 0.13 USD a year earlier)

- Ford Blue revenue: 27.3 billion USD (+4%)

- EBIT: 1.6 billion USD (+100%)

- Ford Pro revenue: 16.2 billion USD (+5%)

- EBIT: 1.6 billion USD (–11%)

- Ford E revenue: 1.4 billion USD (–12%)

- EBIT: –1.4 billion USD (versus a loss of 1.6 billion USD a year earlier)

- Ford Credit revenue: 3.3 billion USD (+6%)

- EBIT: 0.4 billion USD (+33%)

- Total vehicle sales: 530,660 pcs (+1%)

- Electric vehicles: 30,176 pcs (+16%)

- Hybrids: 47,082 pcs (+26%)

- ICE: 453,402 pcs (+7%)

The report reaffirmed that Ford continues to face challenges with electric vehicle margins, with the Ford E segment remaining unprofitable. However, the traditional business of selling internal combustion engine (ICE) vehicles continues to provide support.

Investors reacted negatively to the report, sending the stock price down by 7.5% after its release. The losses in the Ford E division were not a factor, as market participants have already accounted for its weak financial performance. Instead, concerns centred on the company’s 2025 outlook. Despite revenue growth to 48.2 billion USD and net income of 1.8 billion USD, Ford warned of a potential decline in adjusted EBIT to 7.0–8.5 billion USD in 2025, down from 10.2 billion USD in 2024. Another key concern was the possibility of a 25% import tariff on cars from Mexico and Canada, which could adversely affect Ford’s financial results, given the company’s reliance on Mexican plants for low-cost production.

Ford Motor Company Q1 2025 results

Ford released its Q1 2025 financial results on 5 May. The key financial indicators from the report are as follows:

- Revenue: 40.7 billion USD (–5%)

- Net profit: 471 million USD (–65%)

- Earnings per share: 0.12 USD (–64%)

- Ford Blue revenue: 21.0 billion USD (–3%)

- EBIT: 96 million USD (-90%)

- Ford Pro revenue: 15.2 billion USD (+5%)

- EBIT: 1.3 billion USD (–57%)

- Ford E revenue: 1.2 billion USD (+5%)

- EBIT: -849 million USD (compared to a loss of 1.3 billion USD a year earlier)

- Ford Credit revenue: 3.2 billion USD (+6%)

- EBIT: 580 million USD (+78%)

- Total vehicle sales: 501,291 units (–2%)

- Electric vehicles: 22,550 units (+11%)

- Hybrids: 51,073 units (+33%)

- ICE: 427,668 units (–5%)

The Ford Q1 2025 report was mixed, reflecting the increasingly challenging macroeconomic environment for the automaker. Although the company exceeded analysts’ expectations, earning 471 million USD on revenue of 40.7 billion USD, this still represents a 65% decline in net profit compared with the previous year. The 5% drop in revenue and supply chain constraints, exacerbated by new US tariffs, have significantly impacted the results. In response, Ford has suspended the publication of its annual forecast, warning of potential losses of up to 1.5 billion USD due to tariff-related costs. This is a concerning signal, particularly for investors who had counted on stable dividend yields. Amid the uncertainty, Ford may temporarily reduce or even suspend payouts.

Nevertheless, investors reacted moderately positively to the report – following its release, shares rose by 2.7%. This indicates confidence in the company’s ability to adapt, particularly as over 80% of vehicles sold in the US are assembled domestically, which mitigates the impact of tariffs.

Ford’s management expected the first half of the year to be challenging, with EBIT potentially close to zero. An improvement was anticipated in the second half, driven by cost reductions and the launch of new models. However, the EV division remains unprofitable, with a loss of 5 to 5.5 billion USD expected for the full year 2025.

Overall, Ford demonstrated operational resilience, but investors face a choice: either to support the company’s long-term recovery or to wait for greater clarity on tariffs and the outlook for the EV segment.

Ford Motor Company Q2 2025 financial results

Ford released its Q2 2025 financial results on 30 July 2025. Key figures from the report are as follows:

- Revenue: 50.18 billion USD (+5%)

- Net income: 1.50 billion USD (–21%)

- Earnings per share: 0.37 USD (–21%)

- Ford Blue revenue: 25.8 billion USD (–3%)

- EBIT: 661 million USD (–43%)

- Ford Pro revenue: 18.8 billion USD (+11%)

- EBIT: 2.31 billion USD (–10%)

- Ford Model e revenue: 2.4 billion USD (+100%)

- EBIT: –1.3 billion USD (compared with a loss of 1.15 billion USD a year earlier)

- Ford Credit revenue: 3.2 billion USD (+7%)

- EBIT: 645 million USD (+88%)

- Total vehicle sales: 612,095 units (+14%)

- Electric vehicles: 16,438 units (–31%)

- Hybrids: 66,438 units (+23%)

- Internal combustion engine (ICE) vehicles: 529,209 units (+15%)

Ford posted its Q2 2025 financial results with record revenue of 50.2 billion USD and adjusted EBIT of 2.1 billion USD, despite the adverse impact of tariffs amounting to 0.8 billion USD. On a GAAP basis, the company reported a net loss of 36 million USD, driven by special charges related to a 570 million USD vehicle recall and the cancellation of an electric vehicle program. Operating cash flow reached 6.3 billion USD, while adjusted free cash flow was 2.8 billion USD. The Board of Directors confirmed a quarterly dividend of 0.15 USD per share, payable on 2 September.

Management reinstated its full-year guidance, projecting adjusted EBIT between 6.5 and 7.5 billion USD and adjusted free cash flow of 3.5 to 4.5 billion USD, with capital expenditure of around 9 billion USD. The net adverse impact from tariffs was estimated at 2 billion USD, reflecting a total gross effect of 3 billion USD, partially offset by cost-reduction measures amounting to 1 billion USD.

By segment: Ford Pro reported revenue of 18.8 billion USD with an EBIT margin of 12.3%, while the number of paid software and service subscriptions increased by 24% year-on-year to 757,000. Ford Model e revenue doubled to 2.4 billion USD, though the segment incurred an EBIT loss of 1.3 billion USD. Ford Blue reported EBIT of 661 million USD despite a 3% decline in revenue.

Ford Motor Company Q3 2025 earnings results

Ford released its Q3 2025 financial results on 23 October 2025. The key figures are as follows:

- Revenue: 50.53 billion USD (+9%)

- Net profit (non-GAAP): 1.82 billion USD (–7%)

- Earnings per share (non-GAAP): 0.45 USD (–8%)

- Ford Blue revenue: 28.0 billion USD (+7%)

- EBIT: 1.54 billion USD (–5%)

- Ford Pro revenue: 17.4 billion USD (+11%)

- EBIT: 1.99 billion USD (+9%)

- Ford Model e revenue: 1.8 billion USD (+52%)

- EBIT: –1.4 billion USD (compared with a loss of 1.23 billion USD a year earlier)

- Ford Credit revenue: 3.3 billion USD (+7%)

- EBIT: 645 million USD (+16%)

- Total vehicle sales: 545,522 units (+8%)

- Electric vehicles: 30,612 units (+30%)

- Hybrids: 55,177 units (+15%)

- ICE vehicles: 459,733 units (+6%)

Ford reported record quarterly revenue of 50.5 billion USD, with adjusted EBIT of 2.6 billion USD and earnings per share (EPS) of 0.45 USD. Revenue came in slightly above forecasts, while profit was broadly in line with expectations, showing a modest improvement.

The Ford Blue segment (traditional vehicles) generated 28.0 billion USD in revenue and 1.54 billion USD in EBIT profit. The Model e segment increased revenue to 1.8 billion USD but posted a loss of 1.41 billion USD, as the shift to EV production continues to require substantial investment.

Management lowered its full-year guidance, now expecting adjusted EBIT in the range of 6.0–6.5 billion USD, free cash flow between 2.0 and 3.0 billion USD, and capital expenditure of around 9 billion USD. The company warned that the fire at aluminium supplier Novelis would negatively affect Q4 results: the estimated decline in EBIT was 1.5–2.0 billion USD, while free cash flow was expected to decrease by 2–3 billion USD. However, around 1 billion USD of this impact was expected to be recovered in 2026.

Ford Motor Company Q4 2025 earnings results

Ford published its Q4 2025 financial results on 10 February 2025. Below are the key figures from the report:

- *Revenue: 45.90 billion USD (–5%)

#.* Net income (non-GAAP): 528 million USD (–66%)

- *Earnings per share (non-GAAP): 0.13 USD (–67%)

- Ford Blue revenue: 26.2 billion USD (–4%)

- EBIT: 727 million USD (-54%)

- Ford Pro revenue: 14.9 billion USD (–8%)

- EBIT: 1.23 billion USD (–24%)

- Ford Model e revenue: 1.3 billion USD (–9%)

- EBIT: -1.22 billion USD (compared with a loss of 1.40 billion USD a year earlier)

- Ford Credit revenue: 3.4 billion USD (+3%)

- EBIT: 701 million USD (+59%)

- Total vehicle sales: 545,216 units (+3%)

- Electric vehicles*: 14,513 units (–52%)

- Hybrids*: 55,374 units (+18%)

- Internal combustion engine vehicles: 475,329 units (+5%)

Ford’s Q4 2025 report was mixed. Revenue reached 45.9 billion USD, exceeding market expectations. Still, profitability disappointed: adjusted EBIT came in at 1.0 billion USD, and Adjusted EPS was 0.13 USD compared with 0.39 USD a year earlier and below forecasts (which were around 0.17–0.19 USD). Under GAAP, the company reported a net loss of approximately 11.1 billion USD due to substantial one-off charges.

The main reason for the weak GAAP result was 15.5 billion USD in one-off expenses. Of this amount, 10.7 billion USD related to asset impairments and a reassessment of EV programs, while a further 3.2 billion USD was linked to the BlueOval SK project. Excluding these items, the core business remains profitable at the operating level.

The primary profit contributor is the Ford Pro commercial segment (14.9 billion USD in revenue and 1.23 billion USD in EBIT, with an 8.2% margin). Ford Blue generated 727 million USD in EBIT on revenue of 26.2 billion USD. The EV division, Model e, remains loss-making: with revenue of 1.3 billion USD, the EBIT loss amounted to 1.218 billion USD. Ford Credit added 701 million USD in pre-tax profit and supported overall performance.

The company provided relatively confident guidance for 2026: adjusted EBIT of 8–10 billion USD, free cash flow of 5–6 billion USD, and capital expenditure of 9.5–10.5 billion USD. Ford Pro is expected to deliver 6.5–7.5 billion USD in profit, Ford Blue 4.0–4.5 billion USD, while Model e is projected to post a loss of 4.0–4.5 billion USD.

Impact of Trump’s policies on Ford Motor Company

Below are the key valuation multiples for Ford Motor Company based on Q4 2025 results, calculated using a share price of 14 USD.

| Multiple | What it indicates | Value | Commentary |

|---|---|---|---|

| P/E (non-GAAP TTM) | Price paid for 1 USD of earnings over the past 12 months | 12.8 | ⬤ Moderate. The valuation is slightly above Ford’s historical average (typically 7–10x), but remains reasonable in the current market environment, provided earnings recover. |

| P/S (TTM) | Price paid for 1 USD of annual revenue | 0.31 | ⬤ Excellent. Investors pay just 30 cents for every 1 USD of revenue. |

| EV/Sales (TTM) | Enterprise value to sales, accounting for debt | 0.98 | ⬤ Moderate.

A ratio close to 1 is standard for the automotive industry, given its substantial leverage. |

| P/FCF (non-GAAP TTM) | Price paid for 1 USD of free cash flow | 16.09 | ⬤ Moderate. The multiple is within a reasonable range, indicating a moderate ability to convert revenue into free cash flow. |

| FCF Yield (TTM) | Free cash flow yield to shareholders | 6.21% | ⬤ Excellent. A free cash flow yield above 6% allows the company to pay dividends consistently and invest in future development. |

| EV/EBITDA (TTM) | Enterprise value to operating profit before depreciation and amortisation | 21 | ⬤ Weak.

A very high ratio for the industry, indicating that the company is valued richly relative to its operating profit before deductions. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 27 | ⬤ Weak. This confirms low operating efficiency in 2025. |

| P/B | Price to book value | 1.6 | ⬤ Excellent. The market price does not significantly exceed the company’s net asset value. |

| Forward P/E | Forward price-to-earnings (P/E) ratio | 9.94 | ⬤ Excellent. The forward multiple is below the current one, which is a positive signal of earnings growth expectations in the coming year. |

| Net Debt/EBITDA | Debt burden relative to EBITDA | 14.9 | ⬤ Weak.

An extremely elevated ratio. Although a large portion of the debt is tied to Ford Credit, such leverage creates systemic risk in a rising-rate environment. |

| Interest Coverage (TTM) | Ability to cover interest expenses with operating profit | 5.4 | ⬤ Moderate.

A ratio above 3.0 is generally considered safe. Ford remains capable of servicing its debt despite its substantial size. |

Valuation multiples analysis for Ford Motor Company – conclusion

Ford represents a resilient value business undergoing a deep structural transformation. Despite the formal leverage ratios being alarming, they should be interpreted in the context of the company’s capital structure: most of the debt, exceeding 100 billion USD, is concentrated within the Ford Credit division. This debt serves as a self-funded financial services portfolio backed by tangible assets (vehicles) and poses no direct threat to the company’s industrial operations.

The company’s market valuation remains highly conservative, as reflected in its low P/S and P/B ratios, suggesting that investors remain cautious about Ford’s transition to electric vehicles. However, the strong free cash flow yield provides a substantial buffer and supports stable dividend payments. The Forward P/E ratio of 9.94 indicates market expectations of improved operating efficiency and net profit growth in 2026.

Overall, Ford appears undervalued on fundamental revenue and asset-based metrics while retaining the ability to generate stable cash flow even amid volatility. The primary investment appeal currently lies in the combination of Ford Credit’s solid financial foundation and the high-margin Ford Pro division, which together offset the temporary challenges of the Model e segment. The current valuation reflects a balance between the maturity of the traditional business and the risks associated with technological transition, offering investors an attractive return on invested capital at a moderate level of risk.

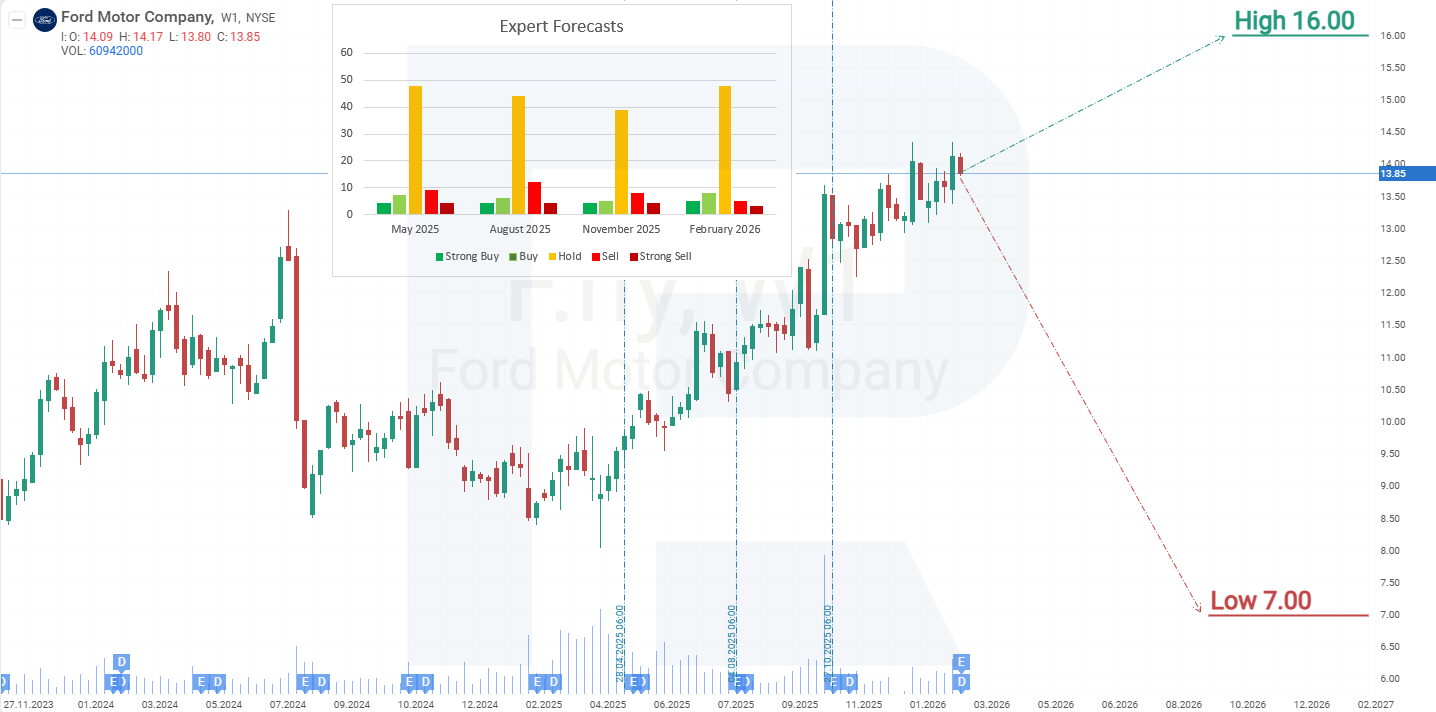

Expert forecasts for Ford Motor Company stock for 2026

- Barchart: 4 out of 22 analysts rated Ford Motor Company shares as a Strong Buy, 15 as Hold, 3 as Strong Sell. The upper price target is 16.00 USD, with the lower bound at 8.00 USD.

- MarketBeat: 4 out of 17 specialists assigned a Buy rating to the shares, 11 recommended Hold, and 2 gave a Sell rating. The upper price target is 16.00 USD, with the lower bound at 7.00 USD.

- TipRanks: 2 out of 15 analysts recommended Buy, 12 recommended Hold, and 1 recommended Sell. The upper price target is 16.00 USD, with the lower bound at 11.00 USD.

- Stock Analysis: 1 out of 15 experts rated the shares as Strong Buy, 2 as Buy, 10 as Hold, and 2 as Sell. The upper price target is 16.00 USD, with the lower bound at 7.00 USD.

Ford Motor Company stock price forecast for 2026

On the weekly chart, Ford shares traded between 8.60 and 13.10 USD from 2022 onwards. In October 2025, F broke above the upper boundary of the range and consolidated above it, increasing the likelihood of further upside. Based on the current performance of Ford Motor Company shares, the possible scenarios for 2026 are as follows:

The base-case forecast for Ford Motor Company stock suggests further growth in F towards resistance at 16.50 USD. If this level is breached, the next upside target would be 20 USD. This scenario is supported by the stock’s attractive dividend yield of 4.6% per annum for long-term investors and the company’s ability to generate stable cash flow even in challenging conditions.

The alternative forecast for Ford Motor Company shares suggests a break below support at 13.10 USD. In this case, F could decline towards the 10.60 USD support level, where a renewed advance may begin, targeting a move back towards 16.50 USD.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.