Amazon (AMZN): post-earnings correction and upside targets for 2026

Amazon reported its Q4 2025 results, with revenue growth and strong AWS momentum. However, the shares fell by 13% following an EPS miss and plans to invest approximately 200 billion USD in 2026.

Amazon.com, Inc. (NASDAQ: AMZN) delivered strong operating results for Q4 2025. Revenue rose to 213.4 billion USD (+14% year-on-year), while its cloud division, AWS, increased revenue to 35.6 billion USD, up 24% year-on-year. The company remains highly profitable: operating income reached 25.0 billion USD, and net income totalled 21.2 billion USD, or 1.95 USD per share, although some figures were affected by one-off factors.

However, market participants reacted negatively to the results. While revenue exceeded analysts’ expectations, earnings per share came in 0.02 USD below forecasts. Additional pressure stemmed from guidance for Q1 2026, with the company expecting revenue of 173.5–178.5 billion USD and operating income of 16.5–21.5 billion USD. Management also announced plans to allocate around 200 billion USD to capital expenditure in 2026, primarily towards AI, cloud infrastructure, and custom chips. This implies that even with solid AWS growth, Amazon will need to spend aggressively to sustain expansion, potentially keeping free cash flow and short-term profitability under pressure.

As a result, a relatively minor EPS miss coincided with a sharp increase in planned AI investment and broader market concerns that technology giants are investing in AI faster than these investments can generate tangible returns. Consequently, pressure was felt not only in Amazon shares but across the wider technology sector.

This article reviews Amazon.com, Inc., provides a fundamental analysis of Amazon’s (AMZN) earnings report, and presents a technical analysis of Amazon.com shares, forming the basis for the AMZN price forecast for 2026. It also examines the company’s business model, assesses the risks of investing in Amazon.com, and outlines expert forecasts for Amazon’s shares.

About Amazon.com, Inc.

Amazon.com, Inc. is one of the world’s largest technology companies. It was established by Jeffrey Bezos in 1994 in Seattle, US. Initially, the company specialised in selling books online but has since evolved into a multi-industry platform. Today, Amazon is engaged in e-commerce, provides cloud computing services through Amazon Web Services (AWS), manufactures electronics (such as Kindle and Echo), and develops media services, including streaming and content production.

The company held its IPO on 15 May 1997, listing its shares on the NASDAQ under the ticker AMZN.

Amazon.com, Inc.’s main financial flows

Amazon’s revenue is based on several key segments, reflecting the company’s varied, multisectoral operations:

- Online retail: selling goods directly on behalf of the company, including books, electronics, clothing, household appliances, and more.

- Marketplace: providing the company’s platform to third-party sellers to sell their goods through its website. Amazon generates revenue from sales commissions, paid storage and delivery services and other seller support services.

- Cloud computing (Amazon Web Services): this is the world’s largest cloud service provider. The service includes server rentals, data storage, big data analytics tools, and other cloud solutions. This segment generates Amazon’s highest profits compared to all other business areas.

- Subscriptions (Amazon Prime and other services): providing access to streaming platforms (video and music), cloud storage, and other products. This category also includes revenue from subscriptions to other services, such as Kindle Unlimited and Amazon Music Unlimited.

- Advertising: actively developing its digital advertising business, including income from placing advertisements on the platform, such as in search results. Revenue from these and other advertising services has increased significantly in recent years.

- Offline retail stores: physical sales outlets, including Amazon Go and Amazon Fresh stores, Whole Foods Market supermarkets, and speciality book and electronics stores.

- Electronics and technology sales: producing and selling its own products, including the popular Kindle eBooks, Echo smart speakers with Alexa voice assistant, Fire TV streaming boxes, and other technology products.

- Other areas: less significant revenue streams, such as providing logistics services to third parties, acting as an intermediary in book publishing (Amazon Publishing), developing video games (Amazon Game Studios), income from the Twitch streaming platform, and other innovative projects.

These diverse revenue streams enable Amazon.com, Inc. to remain resilient to changing market conditions and expand its influence across various sectors.

Amazon.com, Inc. Q3 2024 earnings results

Amazon reported it ended Q3 2024 with gains across key financial indicators. Below is the main report data:

- Revenue: 158.9 billion USD (+11%)

- Net income: 15.3 billion USD (+54%)

- Earnings per share: 1.43 USD (+52%)

- Operating profit: 17.5 billion USD (+55%)

Revenue by segment:

- North America: 95.5 billion USD (+8%)

- Operating income (loss): 5.7 billion USD (+30%)

- International: 35.9 billion USD (+11%)

- Operating income (loss): 1.3 billion USD – in Q3 2023, the company posted a loss of 95 million USD

- Amazon Web Services (AWS): 27.4 billion USD (+19%)

- Operating income (loss): 10.4 billion USD (+49%)

All key financial metrics showed growth in Q3 2024. The international segment saw increased sales, but costs also rose concurrently. As a result, it remained the most vulnerable and could be the first to incur losses in the event of even minor economic disruptions.

The North American segment contributed the most to the company’s total revenue but also incurred the highest costs.

AWS remained Amazon’s most promising and profitable division, demonstrating sustained growth and strong profitability.

For Q4 2024, Amazon forecasts revenue between 181.0 and 188.0 billion USD, representing a 7-11% increase compared to the corresponding period in 2023. Operating profit is expected to range between 16.0 and 20.0 billion USD, up from 13.0 billion USD a year earlier.

Amazon.com, Inc. Q4 2024 earnings results

Amazon reported ending Q4 2024 with growth in key financial metrics once again. The key figures from the report are as follows:

- Revenue: 187.8 billion USD (+10%)

- Net income: 20.0 billion USD (+88%)

- Earnings per share: 1.86 USD (+86%)

- Operating profit: 21.2 billion USD (+60%)

Revenue by segment:

- North America: 115.5 billion USD (+9%)

- Operating income (loss): 9.6 billion USD (+43%)

- International: 43.4 billion USD (+8%)

- Operating income (loss): 1.3 billion USD - In Q4 2023, the company posted a loss of 419 million USD

- Amazon Web Services (AWS): 28.8 billion USD (+19%)

- Operating income (loss): 10.6 billion USD (+48%)

In its commentary on the Q4 2024 report, Amazon’s management provided forecasts for 2025, focusing on revenue, operating profit, and capital expenditures. For Q1 2025, revenue is expected to range between 151.0 and 155.5 billion USD, below the consensus forecast of 158.6 billion USD. Operating profit for this period is projected at 16.0 billion USD, which also falls short of analysts’ expectations.

The company also announced a significant increase in capital expenditures, which could reach 105.0 billion USD in 2025. This marks a notable rise compared to 77.0 billion USD in 2024 and more than double the 48.0 billion USD spent in 2023. These investments will primarily focus on infrastructure, including expanding the AWS cloud business and developing AI solutions.

AWS is anticipated to remain Amazon’s key growth driver in 2025 due to a trend of companies migrating to cloud infrastructure, the end of the cost optimisation phase, and increasing demand for AI solutions. The company has described artificial intelligence as a once-in-a-lifetime opportunity.

The data indicates that Amazon is heavily investing in developing AWS and AI, with substantial investment in infrastructure. However, the weaker-than-expected revenue and operating income forecast for Q1 2025 has disappointed investors, negatively impacting the share price.

Amazon.com, Inc. Q1 2025 earnings results

On 1 May, Amazon.com released its report for Q1 2025, ending 31 March. Below are the key indicators compared to the same period in 2024:

- Revenue: 155.66 billion USD (+9%)

- Net income: 17.12 billion USD (+64%)

- Earnings per share: 1.59 USD (+62%)

- Operating profit: 18.40 billion USD (+22%)

Revenue by segment:

- North America: 92.89 billion USD (+8%)

- Operating income: 5.84 billion USD (+17%)

- International: 33.51 billion USD (+5%)

- Operating income: 1.01 billion USD (+12%)

- Amazon Web Services (AWS): 29.26 billion USD (+17%)

- Operating income: 11.54 billion USD (+22%)

Amazon.com, Inc.’s Q1 2025 earnings report demonstrated solid results, which may attract investors seeking companies with sustainable growth and operational efficiency.

Net sales rose 9% year-on-year despite an adverse currency exchange effect of 1.4 billion USD. This growth was driven by an 8% rise in North American sales and a 5% increase internationally, confirming Amazon’s ability to strengthen its global market position amid economic uncertainty.

A major achievement for the company was the 64% increase in profit and 22% rise in operating profit, reflecting cost optimisation and improved logistics.

Amazon Web Services (AWS), the company’s key profit driver, recorded a 17% increase in sales, reaching an annualised revenue of 117 billion USD. However, it slightly underperformed expectations due to reduced corporate spending amid concerns about tariffs and a potential recession. By comparison, Microsoft Azure, within the Intelligent Cloud segment, grew by 21%, while Google Cloud recorded an even more impressive 28% increase. While AWS maintained its market share leadership (29% in Q1 2025 compared to Microsoft’s 22% and Google’s 10%), it lagged behind its competitors in growth rates, likely due to a higher comparison base and a temporary slowdown in corporate investment in cloud technologies.

Amazon’s online advertising segment grew by 19%, generating 13.92 billion USD, further solidifying its position as the company’s third-largest revenue stream.

However, not everything was positive. The company recorded a 1 billion USD write-down due to product returns and inventory adjustments linked to tariffs. This included 800 million USD in losses from North American retail and 200 million USD in international markets.

AMZN shares fell following the earnings release. The decline was attributed to slower AWS growth and a conservative Q2 2025 forecast, with operating profit expected in the range between 13.0 and 17.5 billion USD, below the consensus estimate of 17.8 billion USD. Management’s caution was linked to tariff policies, particularly the potential 145% duties on Chinese goods, which could affect half of Amazon’s product range. Nevertheless, the forecast appears understated, which could allow the company to exceed expectations if consumer demand remains steady and AWS growth recovers.

While risks remain, including tariff pressures and increased competition in the cloud segment, where Microsoft and Google are accelerating growth. However, Amazon’s competitive advantages in logistics, customer loyalty, and innovation remain significant.

Amazon.com, Inc. Q2 2025 earnings results

On 31 July, Amazon.com released its Q2 2025 results for the period ending 30 June. Below are the key metrics compared with the same period in 2024:

- Revenue: 167.70 billion USD (+13%)

- Net income: 18.16 billion USD (+34%)

- Earnings per share: 1.68 USD (+33%)

- Operating profit: 19.17 billion USD (+30%)

Revenue by segment:

- North America: 100.07 billion USD (+11%)

- Operating income: 7.51 billion USD (+48%)

- International: 36.76 billion USD (+16%)

- Operating income: 1.49 billion USD (+345%)

- Amazon Web Services (AWS): 30.87 billion USD (+17%)

- Operating income: 10.16 billion USD (+9%)

Amazon exceeded expectations for both revenue and profit in Q2 2025 while maintaining high operational efficiency. Revenue grew by 13% to 167.7 billion USD, operating profit reached 19.2 billion USD, and net income came in at 18.2 billion USD, or 1.68 USD per share. The business segments showed divergent performance: AWS added 17.5%, North America grew by 11%, and the international business increased by 16%. Advertising was a key growth driver, with revenue rising by 23% to 15.7 billion USD, supporting monetisation across platforms from the marketplace to Prime Video.

In the second half of the year, the company expected Q3 2025 revenue to range between 174 and 179.5 billion USD, with operating income projected at 15.5 to 20.5 billion USD. Investors perceived this as a cautious outlook, given the high expectations for AI and the cloud.

For the second consecutive quarter, Amazon’s AWS growth lagged behind its competitors. In Q2, AWS revenue grew by 17% year-on-year, but this was noticeably slower than Microsoft Azure (+39%) and Google Cloud (+32%). The main reason for this was the uneven distribution of AI workloads: Azure’s growth is driven by its integration with OpenAI and the AI workloads, while Google Cloud benefits from large deals and the use of AI data.

AWS primarily serves mature corporate clients with traditional cloud services, which means its growth is steady but less impressive than its competitors, who are benefiting from a greater number of new AI use cases. Additionally, Amazon is actively investing in expanding its infrastructure for AI, which increases costs and temporarily reduces margins.

As a result, the slower growth rates do not imply that AWS is losing ground. Amazon is building the necessary infrastructure for AI and gradually scaling up its capabilities.

Amazon.com, Inc. Q3 2025 earnings results

Amazon.com reported its Q3 2025 earnings results on 30 October, covering the period ended 30 September. Below are the key figures compared with the same quarter in 2024:

- Revenue: 180.17 billion USD (+13%)

- Net income: 21.19 billion USD (+38%)

- Earnings per share: 1.95 USD (+37%)

- Operating profit: 17.42 billion USD (0%)

Revenue by segment:

- North America: 106.27 billion USD (+11%)

- Operating income: 4.79 billion USD (–15%)

- International: 40.90 billion USD (+14%)

- Operating income: 1.20 billion USD (–8%)

- Amazon Web Services (AWS): 33.01 billion USD (+20%)

- Operating income: 11.43 billion USD (+9%)

Amazon’s Q3 2025 report came in ahead of analyst expectations. Revenue rose by 13% to 180.2 billion USD, surpassing the market consensus of around 178 billion USD, while earnings per share reached 1.95 USD versus the forecast of roughly 1.56 USD. The company exceeded expectations on both the top and bottom lines. Excluding one-off expenses, the results would have been even stronger. Operating profit totalled 17.4 billion USD; however, this figure included 4.3 billion USD in one-off charges (2.5 billion USD related to FTC litigation and 1.8 billion USD linked to layoffs). Without these items, operating profit would have been approximately 21.7 billion USD, with an operating margin of 12% compared with the reported 9.7%.

Net income increased to 21.2 billion USD (+39% y/y), but a significant portion was attributed to a one-off gain of 9.5 billion USD from the revaluation of Amazon’s stake in Anthropic, unrelated to its core operations.

Performance across segments was also strong: North America revenue grew 11%, international operations expanded 14%, and AWS advanced 20% – its fastest growth rate in the past 11 quarters. AWS maintained a healthy margin of around 35%, while Amazon’s advertising business grew by more than 20%, becoming an increasingly important source of profitability.

Management noted that the company’s key areas – retail, advertising and cloud – continue to see steady demand even amid weak consumer spending. It particularly highlighted the acceleration of AWS growth, driven by demand for AI solutions and continued enterprise cloud migration.

Guidance for Q4 2025 was similarly upbeat: Amazon expected revenue of 206–213 billion USD (+10–13% y/y) and operating profit of 21–26 billion USD. The company also noted that capital expenditure for 2025 will total around 125 billion USD and is expected to rise further in 2026, primarily due to investments in AWS infrastructure, Trainium and Inferentia AI chips, robotics and logistics. Free cash flow declined to 14.8 billion USD owing to increased investments.

Amazon.com, Inc. Q4 2025 earnings results

On 5 February, Amazon.com, Inc. (NASDAQ: AMZN) released its Q4 2025 report for the period ended 31 December. Below are the key figures compared with the same period in 2024:

- Revenue: 213.38 billion USD (+14%)

- Net income: 21.19 billion USD (+6%)

- Earnings per share: 1.95 USD (+5%)

- Operating profit: 24.98 billion USD (+18%)

Revenue by segment:

- North America: 127.08 billion USD (+10%)

- Operating income: 11.47 billion USD (+24%)

- International: 50.72 billion USD (+17%)

- Operating income: 1.04 billion USD (–21%)

- Amazon Web Services (AWS): 35.58 billion USD (+24%)

- Operating income: 12.47 billion USD (+17%)

Amazon’s Q4 2025 report delivered mixed results relative to market expectations. The company reported revenue of 213.4 billion USD, up 14% compared with the same quarter last year and above analysts’ forecasts. Revenue increased across all key segments: retail sales rose, the international business delivered double-digit growth, and Amazon Web Services expanded revenue by 24%, marking its fastest growth in several quarters.

Earnings per share came in at 1.95 USD, slightly below consensus expectations (around 1.97 USD), even though net income in absolute terms increased year-on-year (from 20.00 to 21.19 billion USD).

In its commentary, management emphasised a significant expansion of infrastructure investment, including plans to spend around 200 billion USD in 2026 to support AWS, AI infrastructure, the development of proprietary chips, robotics, and low Earth orbit satellite networks.

Amazon also provided guidance for Q1 2026, forecasting revenue of 173.5–178.5 billion USD and operating income of 16.5–21.5 billion USD, reflecting expectations of continued growth but with a cautious tone, given the seasonal nature of the business and the scale of planned investments.

Investor reaction to Amazon.com, Inc.’s earnings report

Following the publication of Amazon’s Q4 2025 results, investors reacted with a sharp decline in the share price, which also weighed on other technology stocks. Amazon shares fell by 13%, and this drop significantly impacted sentiment across the sector. The decline was driven by several factors related to investor concerns about the company’s prospects.

First, Amazon announced plans to invest around 200 billion USD in capital expenditure in 2026, far exceeding market expectations. Investors perceived this as a risk, as such substantial investments could put pressure on profitability and delay capital returns, particularly if the payback from these investments, such as in AI, materialises slowly.

Second, the company’s capital expenditure growth is significantly outpacing revenue growth in key segments such as AWS. Despite AWS revenue increasing, this growth was not sufficient to justify such a large-scale investment. This reinforced investor concerns that Amazon may be spending too aggressively and too quickly.

In addition, broader market nervousness contributed to Amazon’s share price decline. The technology sector, to which Amazon belongs, has recently experienced a wave of sell-offs, as investors worry that companies committing to large-scale AI investment may struggle to generate adequate returns. Recent data indicate that total AI investment by major technology companies now exceeds 600 billion USD. There are concerns that capital expenditure growth is outpacing these technologies’ ability to generate profit, while the visibility of returns remains limited and uncertain.

Furthermore, rising US government bond yields have made fixed-income instruments more attractive and comparatively safer investments. Taken together, these factors led to a significant decline in Amazon’s share price, with a slight earnings-per-share miss amid rising costs triggering a broader sell-off across the technology sector.

Analysis of key valuation multiples for Amazon.com, Inc.

Below are the key valuation multiples for Amazon.com, Inc. based on Q4 2025 results, calculated using a share price of 208 USD.

| Multiple | What it indicates | Value | Commentary |

|---|---|---|---|

| P/E (TTM) | Price paid for 1 USD of earnings over the past 12 months | 29.3 | ⬤ While the valuation does not appear extreme, the margin of safety remains limited should earnings growth slow. |

| P/S (TTM) | Price paid for 1 USD of annual revenue | 3.1 | ⬤ Moderate for Amazon. |

| EV/Sales (TTM) | Enterprise value to sales, accounting for debt | 3.2 | ⬤ Largely in line with P/S: the capital structure does not materially change the picture, and the valuation remains anchored in expectations for growth and margin expansion. |

| P/FCF (TTM) | Price paid for 1 USD of free cash flow | 292 | ⬤ Very expensive due to sharply compressed free cash flow amid substantial investment spending. |

| FCF Yield (TTM) | Free cash flow yield to shareholders | 0.5% | ⬤Very low. |

| EV/EBITDA (TTM) | Enterprise value to operating profit before depreciation and amortisation | 15.2 | ⬤ Slightly elevated, but justifiable given the quality of AWS and the advertising business. |

| EV/EBIT (TTM) | Enterprise value to operating profit | 28.4 | ⬤ A relatively high price relative to current operating profit. |

| P/B | Price to book value | 5.5 | ⬤ For Amazon, this metric is of secondary importance, but it reflects that the market values the company significantly above its book value. |

| Net Debt/EBITDA | Debt burden relative to EBITDA | 0.35 | ⬤ Low leverage. |

| Interest Coverage (TTM) | Ability to cover interest expenses with operating profit | 35 | ⬤ Interest expenses are covered with a wide margin of safety; rising rates alone are not a key risk factor. |

Valuation multiple analysis for Amazon.com, Inc. – conclusion

Amazon remains strong in terms of profitability and operational resilience: the business generates substantial earnings, and interest payments are comfortably covered. However, from a cash flow perspective, the situation is less comfortable. Due to large-scale investments, free cash flow has declined noticeably, making the P/FCF multiple appear elevated and the FCF yield close to zero. This means that the current share price offers only a limited margin of safety if the market begins to question growth rates or the speed at which major investments will generate returns.

Over the coming year, the decisive factor for Amazon shares will not be profitability itself, but rather AWS dynamics, margins, and free cash flow. If FCF begins to recover, the company’s valuation will look considerably healthier. If not, the risk of a correction driven by multiple contraction remains high.

Expert forecasts for Amazon.com shares for 2026

- Barchart: 49 out of 57 analysts rated Amazon shares as Strong Buy, 5 as Moderate Buy, and 3 as Hold. The upper price target is 360 USD, with the lower bound at 175 USD.

- MarketBeat: 55 out of 59 analysts assigned a Buy rating to the shares, with 4 recommending Hold. The upper price target is 360 USD, with the lower bound at 175 USD.

- TipRanks: 41 out of 44 professionals recommended Buy, with 3 advising Hold. The upper price target is 325 USD, with the lower bound at 175 USD.

- Stock Analysis: 20 out of 45 experts rated the shares as Strong Buy, 23 as Buy, and 2 as Hold. The upper price target is 325 USD, with the lower bound at 175 USD.

Amazon.com, Inc. stock price forecast for 2026

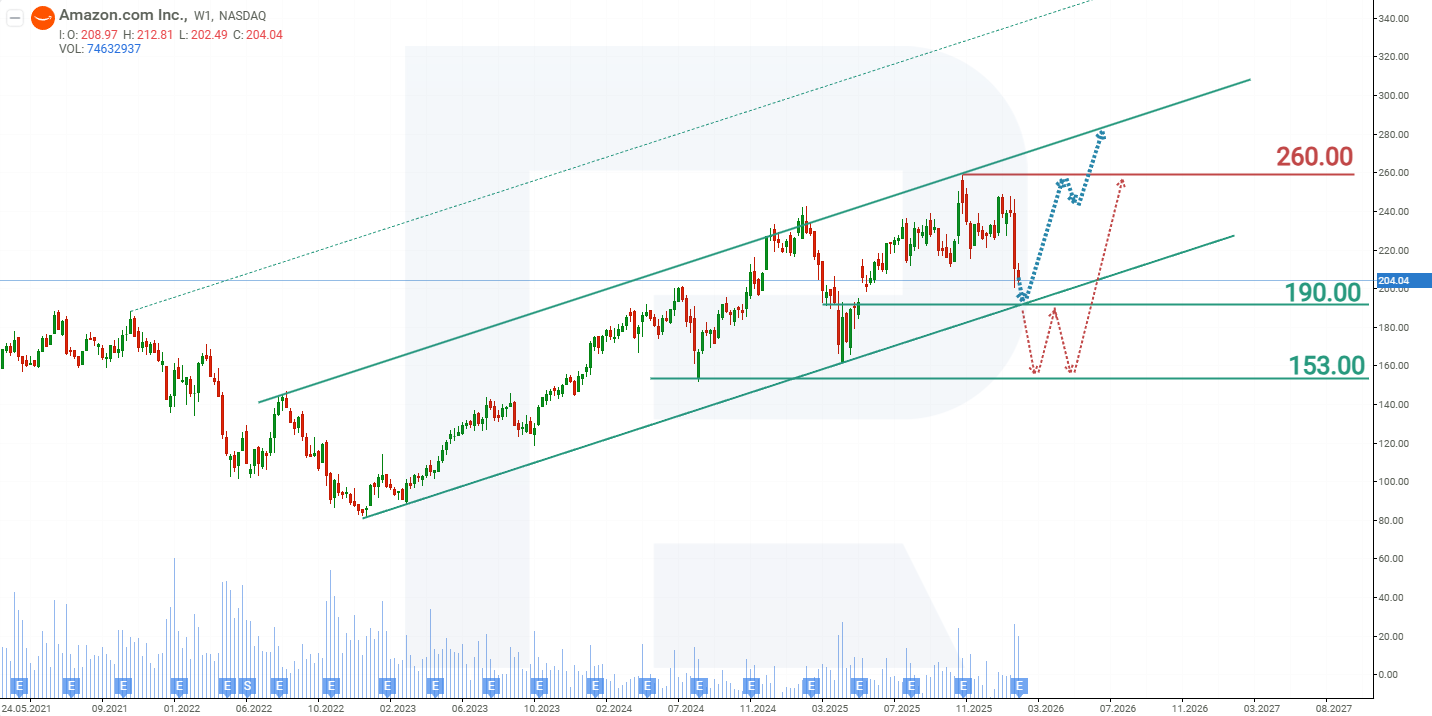

On the weekly chart, Amazon.com (AMZN) shares are trading within an ascending channel. Following the publication of the Q4 2025 report, the share price moved lower; however, this decline remains within the bounds of a correction inside the broader uptrend. The nearest support is at 190 USD, which also aligns with the ascending trendline, reinforcing this level as a key support area. Based on Amazon.com’s current stock performance, the possible scenarios for 2026 are as follows:

The base-case forecast for AMZN shares suggests a test of support at 190 USD, followed by a rebound and a resumption of growth within the ascending channel. The first upside target would be the 260 USD resistance level. If this level is breached, the next target would be the upper boundary of the channel at 290 USD.

The alternative forecast for AMZN shares foresees a break below the 190 USD support level. In this scenario, the share price could decline towards 153 USD, where a consolidation range may form, followed by a potential resumption of the upward move.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.